Stocks You Shouldn’t Own

By OSAM Research Team

January 2016

Active management has two potential advantages versus an index. The first advantage is the one that most people think of: active stock selection. But this paper instead focuses on the second potential advantage: active stock elimination, or identifying stocks not to own in the portfolio. While owning strong performers is the most obvious source of excess returns versus a benchmark, the stocks that are in an index but not in an active portfolio often explain as much of the active portfolio’s relative returns.

In 2015 for example, not owning Exxon, Chevron, Berkshire Hathaway, or Kinder Morgan was a large advantage relative to the major U.S. market indexes. Stocks as big as Exxon or Berkshire Hathaway have a large impact on the return of index-based funds. This is true regardless of the current quality or valuation of these stocks. This is a weakness that disciplined active approaches can exploit.

One interesting side effect of the rise of index funds is that every stock in any major index fund receives a constant bid in the market as more and more net cash flows into the major index funds and ETFs. When an investor buys SPY, the largest index ETF, they do not do so thinking that Kinder Morgan (or Exxon, or Amazon) is a good buy. They are instead simply betting on the market’s overall appreciation and dividends. But their buying decision creates demand for Kinder Morgan’s shares indirectly and, if and when there are negative net flows out of index funds, creates selling pressure. This upward pressure happens regardless of current quality.

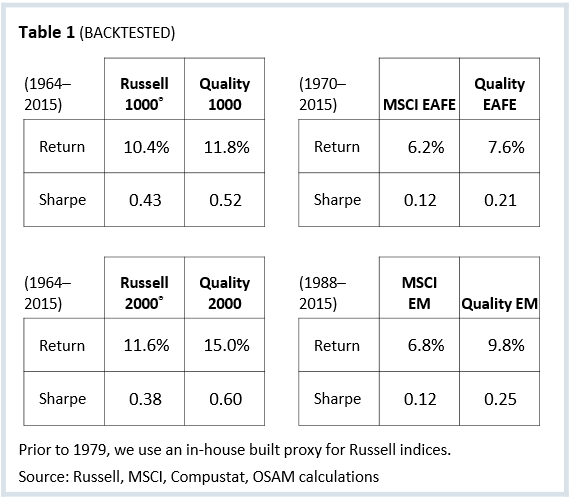

But as we shall see, quality should not be ignored. A simple test removing the lowest quality stocks from common indexes (U.S. Large Cap, U.S. Small Cap, Developed International, and Emerging markets) shows that using quality as a filter in the investment process could have improved annual returns by an average of 2.3 percent annually.

In Table 1, we show the historical results for a group of “modified” higher quality indexes. These quality indexes use the same stocks, the only difference is that we remove the lowest 50 percent of stocks in each universe by three measures of quality, which we explore further in this paper. Once removed, we weight the remaining stocks by their float-adjusted market cap, just as the index would. Table 1 displays the results.

We do not advocate cap-weighting. Nor do we advocate a simple approach like the one shown above. Instead, we believe that certain stocks should be removed from consideration using certain quality metrics. These results demonstrate the potential power of not owning certain stocks, even in the existing cap-weighted index framework.

We believe that in the age of indexing, active strategies should first work hard to remove the poorest quality stocks from consideration entirely, regardless of their weight in the index. Size alone—the driver of a stock’s weight in SPY and other index funds—is not a sufficient reason for owning a stock. Below we define what we mean by quality and show how it can significantly improve any investing process.

What is Quality?

“Quality” means different things to different investors. We use quality as a negative screen: to avoid stocks rather than to select them. Specifically, we find that factors that measure Financial Strength, Earnings Growth, and Earnings Quality are the most effective ways to objectively remove stocks from consideration for investment.

With our Financial Strength factor, we evaluate a company’s sources of financing and leverage. We find companies that are more reliant on external financing, particularly those with significant recent growth in total debt, and have low cash flows relative to their total debt, tend to underperform the market.

We evaluate a company’s recent earnings with our Earnings Growth factor. The value of equity is based on the future earnings that company will generate. Companies with low levels of profitability, falling earnings, and negative recent earnings surprises have tended to underperform the market.

Earnings Quality identifies companies that are aggressively-reporting or misrepresenting their earnings. Accounting choices can inflate earnings by delaying expenses or recognizing revenue early, but these actions create an imbalance in the financial statements. We avoid companies with high and rising accruals (non-cash items), atypical growth in their assets, and low depreciation costs relative to capital investment. We have found that companies that are aggressively manipulating their earnings cannot sustain it forever and tend to underperform in the future.

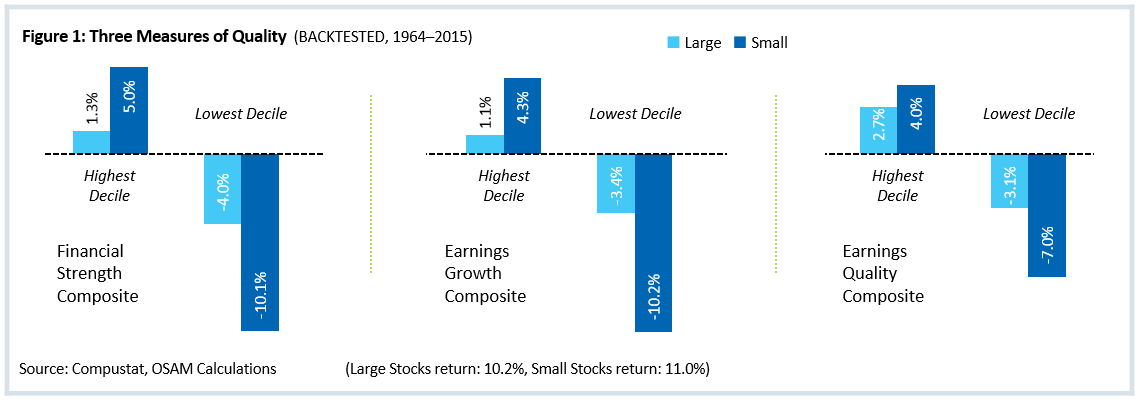

Collectively, we believe that these three measures of quality can help eliminate poor performers from the investible universe, regardless of their weight in a given market index. The historical data suggests that, no matter a company’s size, if it is among the lowest stocks in the market by financial strength, earnings quality, or earnings growth, it should be avoided. Figure 1 (below) shows the returns of the highest and lowest decile by each factor.

To see how these themes manifest in the real market, the following pages include two historical examples where using quality factors could have helped investors avoid bad investments.

Dot-Com Stocks in 1999

As the internet took off, the prime focus was on building revenue and attracting users, without a focus on basic business principles like profitability. In the race to build revenue, several companies raised capital and burned through it at unsustainable rates, ending with their operating model falling apart.

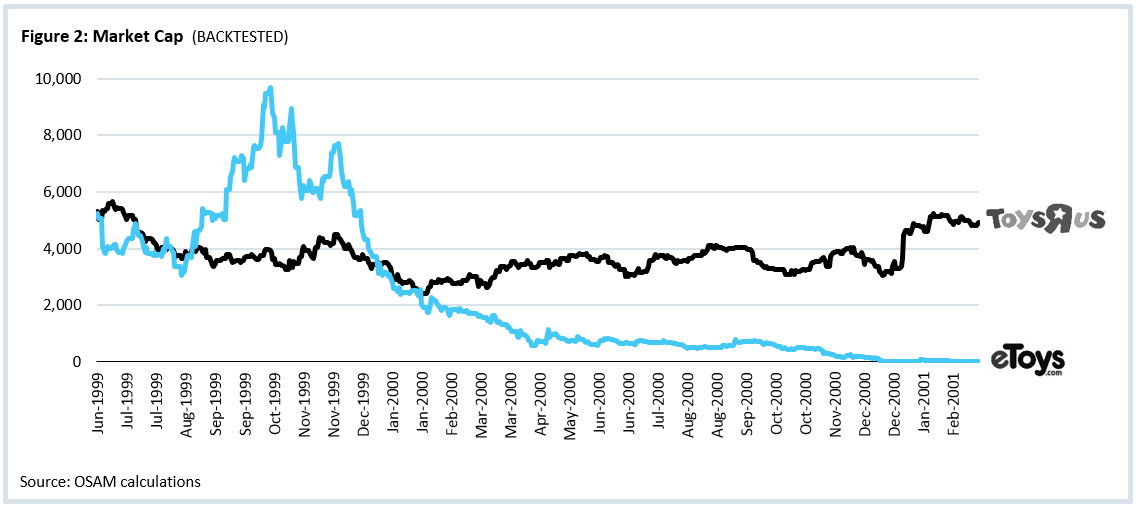

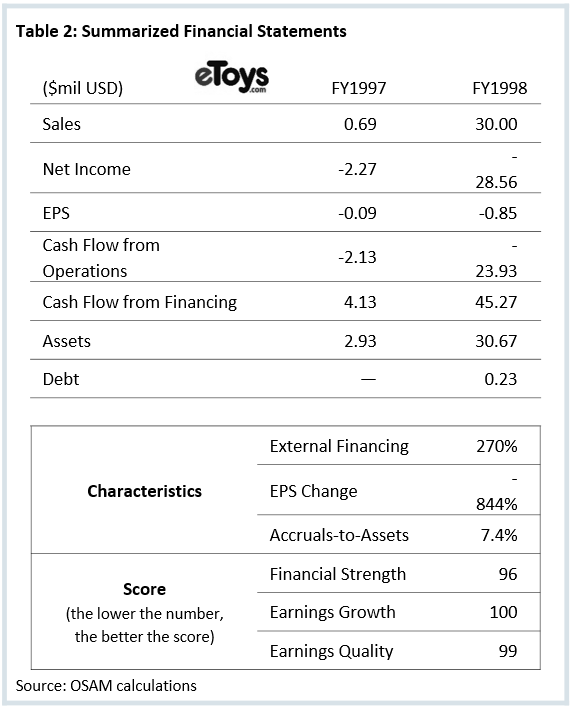

One of the most salient examples was eToys. The online retailer was the first to specifically target the $22 billion toy market, beating the brick and mortar Toys "R" Us to the online market by over a year. The site launched in October 1997. In its first fiscal year, it generated modest revenue of almost $700,000. By the next year, it had generated $30 million in revenue. This is significant growth, and made the company the third largest online retailer, trailing only Amazon and Barnes & Noble.

eToys had an initial public offering in 1999. The stock was listed at $20 but by the end of the day, the stock price had climbed to $77. Valuation peaked in late October 1999, giving it a market cap close to $9 billion―over two and a half times Toys "R" Us―making it the 64th largest company on the NASDAQ exchange. Think about how astonishing that is: eToys had revenues of $30 million versus sales at Toys "R" Us of $11 billion, yet eToys had the higher overall valuation and would have qualified for the NASDAQ 100.

For the fiscal year 1998, the sales grew, but the company spent almost two dollars for every single dollar of revenue to capture market share. eToys spent $5 million to become a preferred retailer on AOL and entered a similar deal with Yahoo! The aggressive spending caused earnings to decline by -844 percent. As earnings fell, the company was funding itself from financing instead of operating activities by issuing equity. Cash taken in from external sources (new equity, debt) was 2.7 times that of the value of the company’s existing assets. Under pressure to represent itself as more desirable to investors, the company also used accounting tricks to improve earnings: accruals (non-cash earnings) measuring 7.4 percent of its asset base.

This is exactly the profile that we designed our quality metrics to avoid: a company with declining earnings that was propping them up through accounting, while financing itself through equity instead of operations. While eToys’ stock price was doing well, its quality—measured through our three quality scores—was at the bottom of the market: its Financial Strength was in the 96th percentile (100 is the lowest), its Earnings Growth was in the 100th, and Earnings Quality in the 99th.

The outcome of eToys was well publicized. After a disappointing Christmas in 2000, the stock halted trading on February 26, 2001 as it was unable to meet the minimum requirement of trading at $1 per share for 30 days. The stock closed at $0.09. The company that once had a $9 billion market capitalization was sold off in parts for less than $20 million.

Telecom Meltdown in 2002

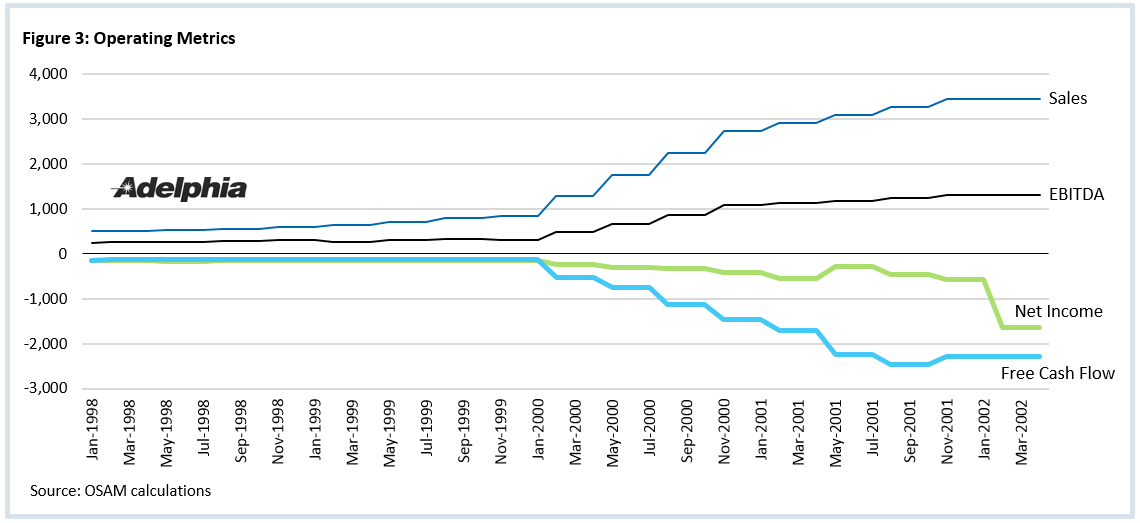

Right on the heels of the dot-com crash was the Telecom Meltdown in 2002. By the end of 2002, Telecom investors had lost $2 trillion in capital, double the losses of the dot-com crash. The Rigas family treated their company Adelphia—which was once the sixth largest cable-television company—like a private bank account. Their looting ranged from smaller purchases like massages and family safaris, to large ones such as funding the purchases of hockey teams and golf courses through off-balance-sheet entities. After a 20-month investigation, three years of financial statements had to be restated and several members of the Rigas family went to prison. Quality factors would have identified issues early.

Starting in 1999, some basic operating metrics started to deteriorate. While overall sales tripled from 1999 to 2002, operating cash flow growth as measured through EBITDA significantly lagged. It would later be discovered that the Rigas family created shell corporations that would be used to artificially boost sales and EBITDA. Yet, cash flows as measured through net income and, notably free cash flow, deteriorated at the same rate sales were burgeoning.

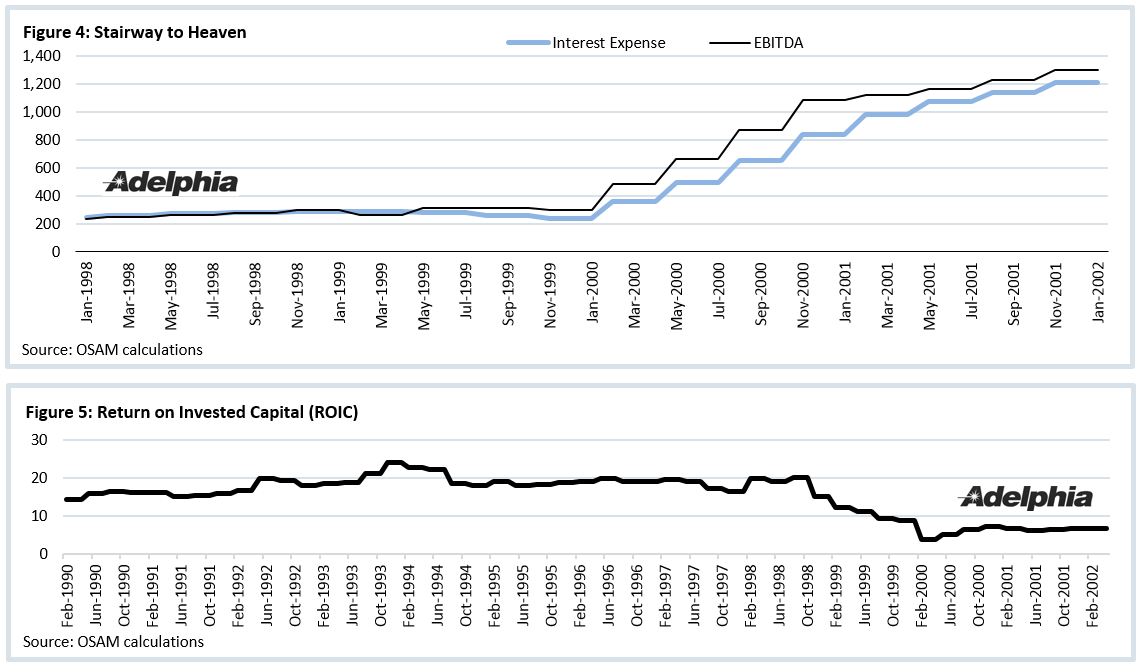

By year end 2000, the company was issuing the equivalent of 30 percent of its assets in debt and equity to finance acquisitions and hide the cash drain. As debt piled on the balance sheet, interest expense grew in lock step with EBITDA. Effectively, all of the company’s cash flow, real and fabricated, was going to pay debt holders.

The problem with fabricated assets is that they are not productive. Return on Invested Capital crumbled as a result.

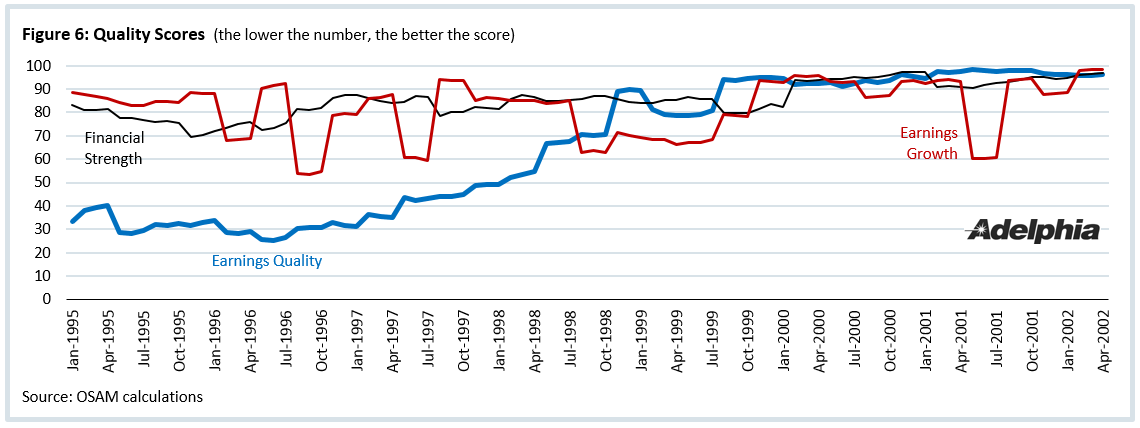

There were many red flags with Adelphia. Here are the three quality scores for the stock between 1995 and 2002. In each case, the closer the score to 100 the worse the quality of the company is relative to all other stocks trading in the market. You can see Adelphia’s Earnings Quality score (blue) steadily worsen, eventually matching the already bad Financial Strength and Earnings Growth trends. All three scores—which would have quickly removed Adelphia’s stock from consideration—presaged Adelphia’s eventual bankruptcy.

The Impact of Quality

History has several more bankruptcies like eToys and Adelphia. US Airways in the post-9/11 meltdown, WCI Communities in the real estate collapse of 2008, or more recently Eclipse Resources in 2015 with the collapse in oil prices. These and several more companies all exhibited the warning signs of poor quality. Major indexes pay no consideration to Financial Strength, Earnings Quality, or Earnings Growth. At their peak, eToys and Adelphia each would have been within the largest 100 companies on the NASDAQ, based solely on the size of their market cap. If indexes screened for quality to remove stocks like eToys and Adelphia, their historical results would have been very different—and much better for equity holders.

You can build a winning strategy directly and indirectly. You can win directly by identifying and buying stocks that are poised to outperform using factors like valuation and shareholder yield. This is a central part of our investment process. But you can also win indirectly, by identifying stocks that have suspect Financial Strength, Earnings Quality, and Earnings Growth and removing them from consideration. A broad index—or even many enhanced “smart” indexes—will own everything. By not owning the lowest quality stocks, we believe active investors can improve their odds of success.

General Legal Disclosures & Hypothetical and/or Backtested Results Disclaimer

The material contained herein is intended as a general market commentary. Opinions expressed herein are solely those of O’Shaughnessy Asset Management, LLC and may differ from those of your broker or investment firm.

It should not be assumed that your account holdings correspond directly to any comparative indices. Individual accounts may experience greater dispersion than the composite level dispersion (which is an asset weighted standard deviation of the accounts in the composite for the full measurement period). This is due a variety of factors, including but not limited to, the fresh start investment approach that OSAM employs and the fact that each account has its own customized re-balance frequency. Over time, dispersion should stabilize and track more closely to the composite level dispersion. Gross of fee performance computations are reflected prior to OSAM’s investment advisory fee (as described in OSAM’s written disclosure statement), the application of which will have the effect of decreasing the composite performance results (for example: an advisory fee of 1% compounded over a 10-year period would reduce a 10% return to an 8.9% annual return). Portfolios are managed to a target weight of 3% cash. Account information has been compiled by OSAM derived from information provided by the portfolio account systems maintained by the account custodian(s), and has not been independently verified. In calculating historical asset class performance, OSAM has relied upon information provided by the account custodian or other sources which OSAM believes to be reliable. OSAM maintains information supporting the performance results in accordance with regulatory requirements. Please remember that different types of investments involve varying degrees of risk, that past performance is no guarantee of future results, and there can be no assurance that any specific investment or investment strategy (including the investments purchased and/or investment strategies devised and/or implemented by OSAM) will be either suitable or profitable for a prospective client’s portfolio. OSAM is a registered investment adviser with the SEC and a copy of our current written disclosure statement discussing our advisory services and fees continues to remain available for your review upon request.

Hypothetical performance results shown on the preceding pages are backtested and do not represent the performance of any account managed by OSAM, but were achieved by means of the retroactive application of each of the previously referenced models, certain aspects of which may have been designed with the benefit of hindsight.

The hypothetical backtested performance does not represent the results of actual trading using client assets nor decision-making during the period and does not and is not intended to indicate the past performance or future performance of any account or investment strategy managed by OSAM. If actual accounts had been managed throughout the period, ongoing research might have resulted in changes to the strategy which might have altered returns. The performance of any account or investment strategy managed by OSAM will differ from the hypothetical backtested performance results for each factor shown herein for a number of reasons, including without limitation the following:

- Although OSAM may consider from time to time one or more of the factors noted herein in managing any account, it may not consider all or any of such factors. OSAM may (and will) from time to time consider factors in addition to those noted herein in managing any account.

- OSAM may rebalance an account more frequently or less frequently than annually and at times other than presented herein.

- OSAM may from time to time manage an account by using non-quantitative, subjective investment management methodologies in conjunction with the application of factors.

- The hypothetical backtested performance results assume full investment, whereas an account managed by OSAM may have a positive cash position upon rebalance. Had the hypothetical backtested performance results included a positive cash position, the results would have been different and generally would have been lower.

- The hypothetical backtested performance results for each factor do not reflect any transaction costs of buying and selling securities, investment management fees (including without limitation management fees and performance fees), custody and other costs, or taxes – all of which would be incurred by an investor in any account managed by OSAM. If such costs and fees were reflected, the hypothetical backtested performance results would be lower.

- The hypothetical performance does not reflect the reinvestment of dividends and distributions therefrom, interest, capital gains and withholding taxes.

- Accounts managed by OSAM are subject to additions and redemptions of assets under management, which may positively or negatively affect performance depending generally upon the timing of such events in relation to the market’s direction.

- Simulated returns may be dependent on the market and economic conditions that existed during the period. Future market or economic conditions can adversely affect the returns.