Microcap as an Alternative to Private Equity

By Chris Meredith, Patrick O’Shaughnessy

December 2017

Private equity (PE) has become a central component of many institutional and high-net-worth investment portfolios over the past decade. While private equity offers potential advantages, it also requires taking distinct risks. This paper highlights an alternative to private equity—microcap equities—which mitigates several of these risks.

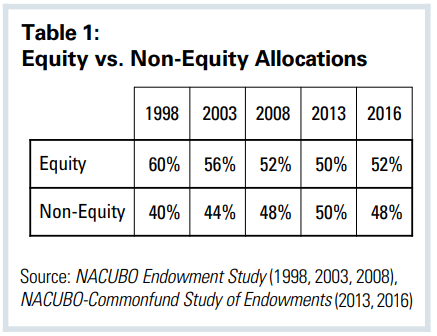

Institutional investors have changed their asset allocation over the past 18 years. The allocation to equities decreased slightly, down 8 percent overall in those 18 years, but the split between private and public equity shifted dramatically, with private equity rising on average from 1.4 percent to 17.0 percent.

Private equity offers several advantages, including:

Access to smaller companies

Small companies at the start of their business have higher growth opportunities. With the overall economy slowing down, investors are searching for growth—private equity can offer attractive growth opportunities compared to large cap public equities. While some private equity funds invest in larger businesses, the access they provide to smaller businesses is a distinct advantage.

Diversification

The investment companies in a private equity fund are excluded from the investment universe and also from the benchmarks of public equity managers.

Total return

The published returns of private equity look more attractive than public equities. The reason most commonly cited for PE’s higher returns is that investors are capturing an “illiquidity premium.”

As we shall see, microcap equities provide similar advantages but without the baggage of illiquidity, highly uneven returns, and higher, more complicated fees. Let’s look at these three key disadvantages of private equity investments.

Illiquidity

Private equity investments require as much as a 10-year commitment, with an initial up-front payment and capital calls over the first several years. This capital is deployed into private investments that are held for several years, and gains are returned as those profits are realized through liquidity events. The private equity manager fully determines these liquidity events, which presents issues for plan sponsors in redeploying cash and forecasting portfolio cash flows.

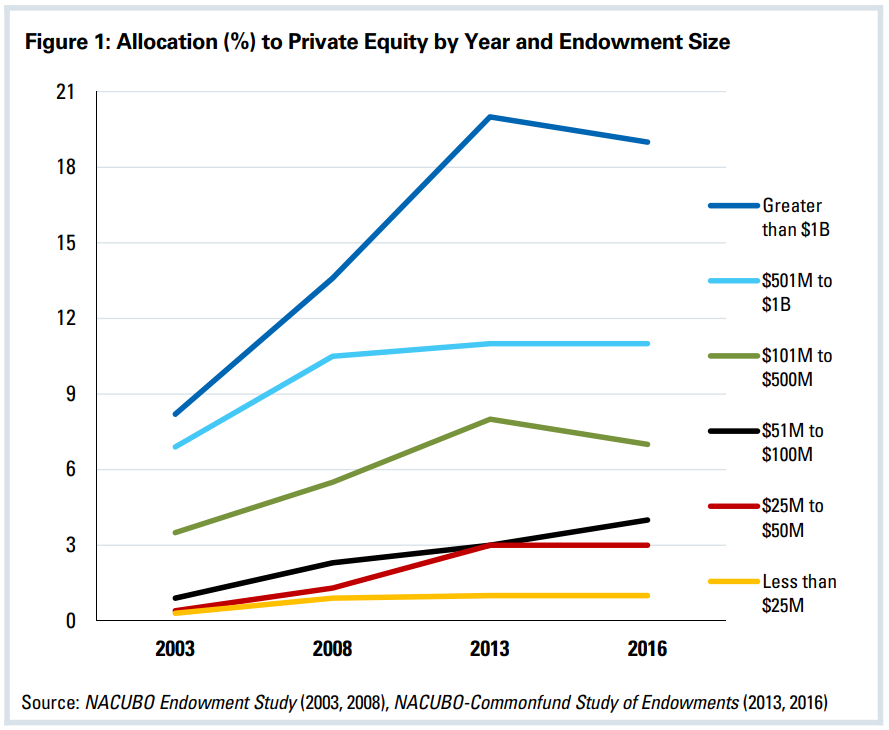

For a long-term investor, this seems like a reasonable trade for higher returns. But, for many investors, low liquidity means private equity is often too restrictive. For example, many endowments have been unable or unwilling to build their allocation to the asset class. Data from the NACUBO-Commonfund Study of Endowments shows that the increased allocation to private equity has been driven by the largest endowments (see Figure 1 below).

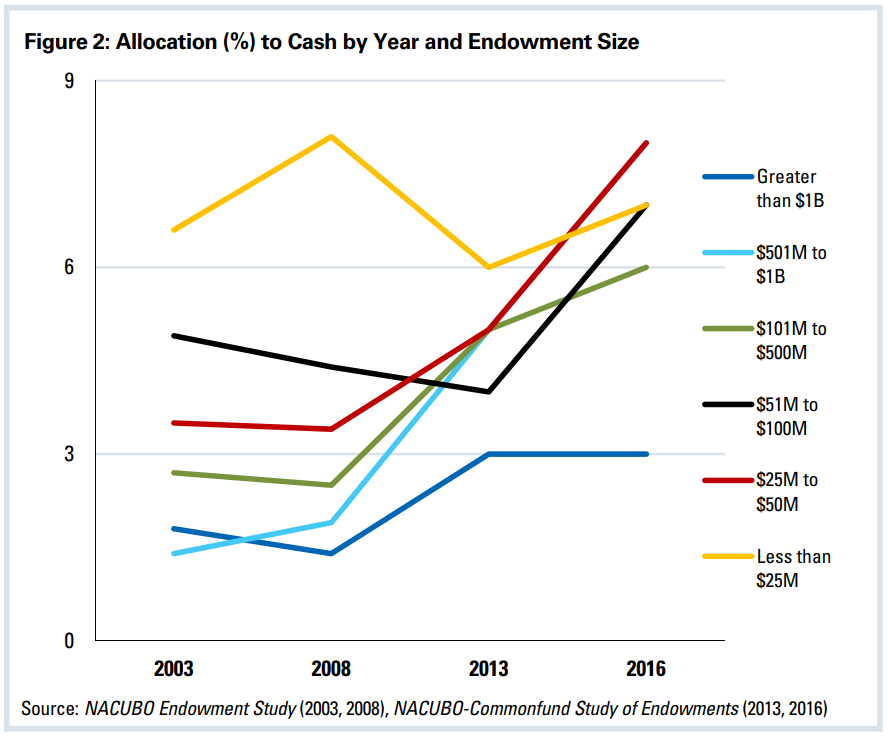

At the same time, smaller endowments have had much higher average allocations to cash, highlighting the need for (or concerns about) short-term liquidity within the portfolio.

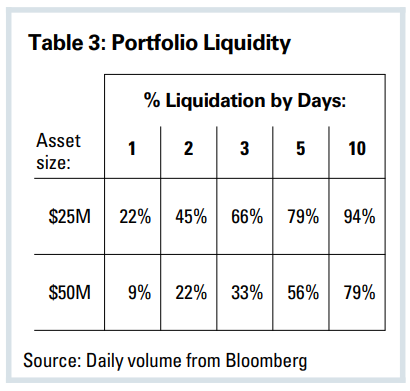

Microcap public equities are less liquid than their larger cap counterparts, but they are still very liquid relative to private equities. Most microcap portfolios can be liquidated in short order. Table 3 (above) shows the estimated time to liquidate microcap portfolios of $25M and $50M, assuming an investment in our microcap model portfolio as of June 2017. These results assume we participate in 25 percent of each day’s trading volume for each individual stock. The vast majority of these portfolios could be liquidated within a week—a far cry from the multi-year lockup required by many private equity funds.

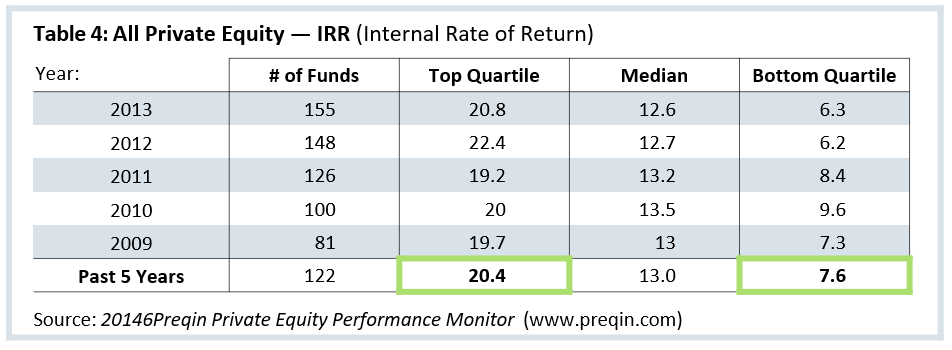

Private Equity Managers Have More Uneven Returns

While private equity offers the prospect of great returns, the historical results for managers in the asset class have been uneven. Reporting returns for illiquid portfolio companies is difficult, but even if the stated returns of private equity managers accurately reflect the valuation of their holdings, private equity managers still show wide dispersion in their ability to generate consistent returns.

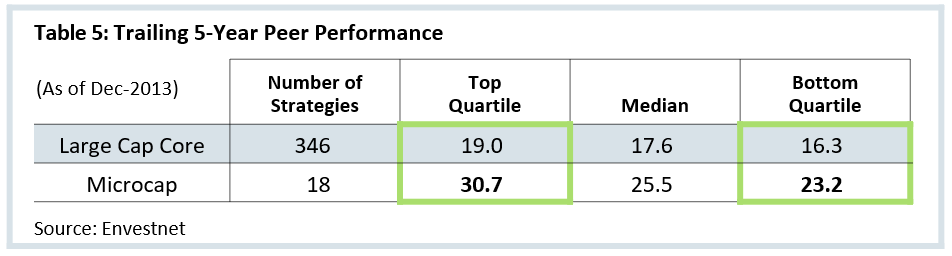

Table 4 (below) compares the dispersion between the top and bottom quartile performers over the past five years for equity managers both private and public.

Such high dispersion makes access to top managers a critical component in establishing a private equity allocation—but identifying those managers ahead of time is difficult. The highest quartile private equity manager had a five-year return of 20.4 percent, which is nearly 3⨉ higher than the return for the lowest quartile manager (7.6 percent). In contrast, the highest quartile microcap manager had a return of 30.7 percent—just 1.3⨉ the return earned by the bottom quartile manager (23.2 percent).

Fees

Taken together, these issues around illiquidity and uneven returns raise concerns about allocations to private equity in the coming decade. But perhaps the most notable difference between private equity and microcaps are the fees required to access the market. As John Bogle is fond of saying, “In investing, you get what you don’t pay for.” Private equity funds can charge capital on three types of assets: committed capital, called capital, and invested assets (including leveraged assets). A flat fee to access the microcap market is likely lower—and less complicated—than private equity fees. These cost savings compound to significant amounts over time.

The Alternative: Microcap Equity

Microcap public equities provide the same advantages as allocations to private equity, and do so without some of the baggage associated with private equity. With microcaps, there are few concerns about accurately measuring returns or multi-year illiquidity—and fees are significantly lower.

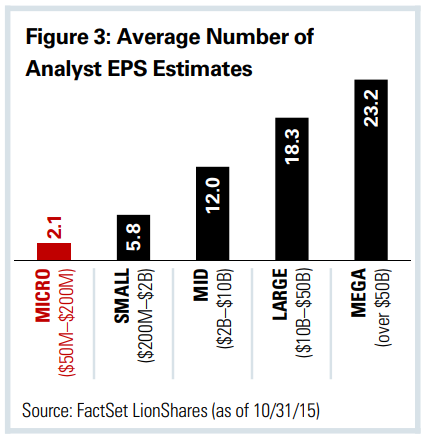

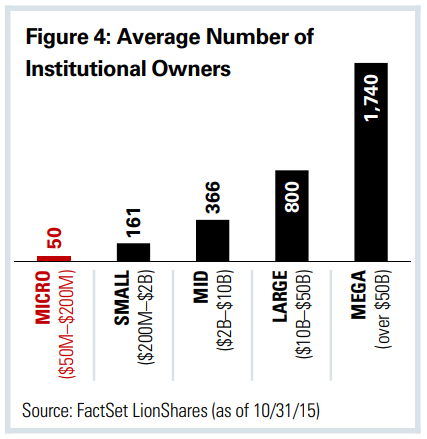

The total market cap of the microcap space, which we define as one having a market cap between $50M and $200M, is $146B—roughly the same size as The Walt Disney Company’s market cap. This means that micro-caps are a scarce opportunity, which is good because larger institutional asset managers (and, in turn, Wall Street) often neglect them. The typical microcap stock is only covered by 2.1 analysts on average, and many have no analyst coverage at all. Additionally, whereas the largest cap public equities have an average of 1,740 different institutional owners, microcaps only have an average of 50. The lack of attention to these stocks offers up a greater chance to find attractive investments.

How to Invest in Microcaps

Microcaps themselves often earn higher returns than the broader equity market. For the five years ending March 2014 (see Table 5 below), the median microcap manager outperformed the median large cap manager by 7.9 percent annualized.

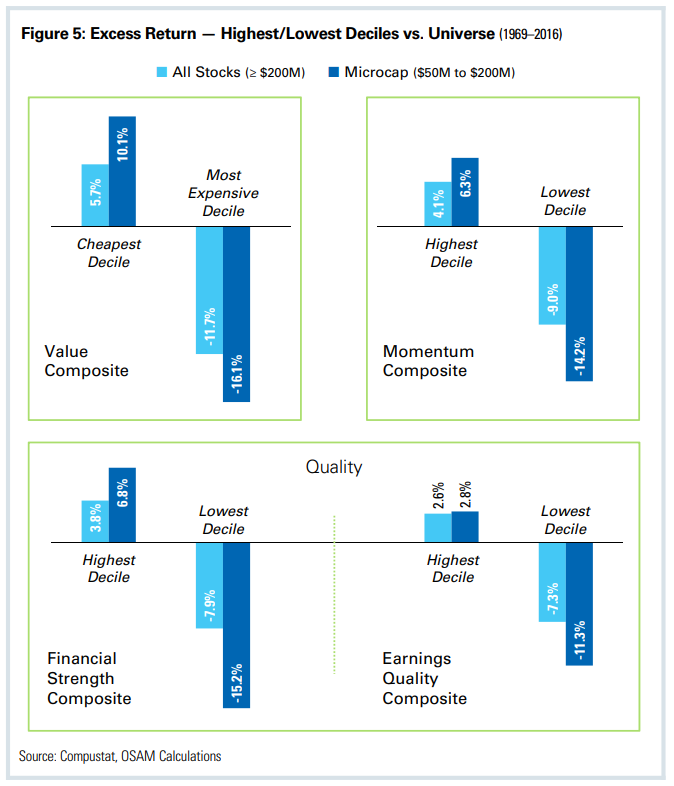

But the real advantage of investing in microcaps is systematically buying stocks with very cheap valuations, high-quality balance sheets and earnings, and strong recent price trends (momentum). These themes—Value, Quality, Financial Strength, and Momentum—have worked even in the largest cap portion of the public equity markets. And they are much more effective and predictive in the microcap market, which is neglected and therefore less efficient.

Here is how we measure these key stock selection themes:

VALUE

We favor stocks that trade at cheap multiples of their sales, earnings, free cash flows, and EBITDA. We also favor companies with higher shareholder yields (dividends + net buybacks). Though shareholder yield is less common for microcap stocks, we still favor those companies that are buying back shares while avoiding the ones that are issuing large amounts of new equity.

MOMENTUM

We favor stocks with strong recent price trends. Those stocks that have been strong relative performers over the past three to nine months tend to continue to outperform the market.

FINANCIAL STRENGTH

We favor stocks with higher-quality balance sheets, meaning reasonable amounts of leverage, strong cash flows to support debt, and low reliance on external sources of financing.

EARNINGS QUALITY

We favor stocks with conservative principles in reporting earnings, meaning low accruals and conservative accounting choices (e.g., high depreciation-to-capital expenditures).

In Figure 5, we show the historical excess return (1969–2016) earned by the highest and lowest deciles of stocks ranked by Value, Quality, and Momentum. We show these results in two universes: All Stocks ($200M market cap and higher) and Microcaps ($50M to $200M).

SUMMARY

Because the total value of all microcaps is small, its market represents a scarce investment opportunity (we estimate total capacity at a few hundred million dollars). But for those who are able to take a position, microcap equities can solve the original goals of private equity while eliminating investment issues associated with the asset class:

Better liquidity

A microcap portfolio can be liquidated in short order—in part or in full. Private equity investments are far less liquid.

Access to smaller high-growth companies

Similar to companies in private equity portfolios, many microcap companies are in the very early (and high growth) stages of their development. These companies have the potential to deliver higher returns than established large cap equities.

Diversification

Like private equity, microcap portfolios have little to no overlap with the constituents of larger public equity benchmarks.

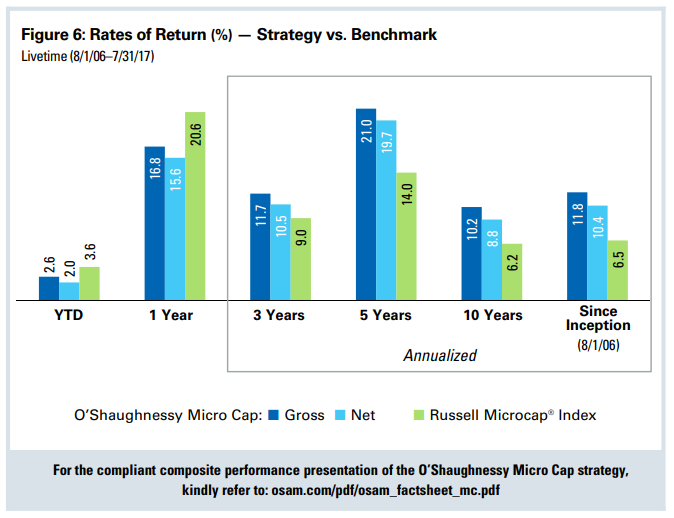

Strong returns

While the asset class itself offers attractive returns, a strategy that focuses only on those microcap stocks with outstanding quality, valuation, and momentum offers even better prospective returns. Shown to the right are the live historical results (2006–present) of the O’Shaughnessy Micro Cap strategy versus its benchmark.

Given its potential benefits, microcap equities can be a critical piece of a diversified portfolio.

General Legal Disclosures & Hypothetical and/or Backtested Results Disclaimer

The material contained herein is intended as a general market commentary. Opinions expressed herein are solely those of O’Shaughnessy Asset Management, LLC and may differ from those of your broker or investment firm.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by O’Shaughnessy Asset Management, LLC), or any non-investment related content, made reference to directly or indirectly in this piece will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this piece serves as the receipt of, or as a substitute for, personalized investment advice from O’Shaughnessy Asset Management, LLC. Any individual account performance information reflects the reinvestment of dividends (to the extent applicable), and is net of applicable transaction fees, O’Shaughnessy Asset Management, LLC’s investment management fee (if debited directly from the account), and any other related account expenses. Account information has been compiled solely by O’Shaughnessy Asset Management, LLC, has not been independently verified, and does not reflect the impact of taxes on non-qualified accounts. In preparing this report, O’Shaughnessy Asset Management, LLC has relied upon information provided by the account custodian. Please defer to formal tax documents received from the account custodian for cost basis and tax reporting purposes. Please remember to contact O’Shaughnessy Asset Management, LLC, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you want to impose, add, or modify any reasonable restrictions to our investment advisory services. Please Note: Unless you advise, in writing, to the contrary, we will assume that there are no restrictions on our services, other than to manage the account in accordance with your designated investment objective. Please Also Note: Please compare this statement with account statements received from the account custodian. The account custodian does not verify the accuracy of the advisory fee calculation. Please advise us if you have not been receiving monthly statements from the account custodian. Historical performance results for investment indices and/or categories have been provided for general comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your account holdings correspond directly to any comparative indices. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. O’Shaughnessy Asset Management, LLC is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice. A copy of the O’Shaughnessy Asset Management, LLC’s current written disclosure statement discussing our advisory services and fees is available upon request.

The risk-free rate used in the calculation of Sortino, Sharpe, and Treynor ratios is 5%, consistently applied across time.

The universe of All Stocks consists of all securities in the Chicago Research in Security Prices (CRSP) dataset or S&P Compustat Database (or other, as noted) with inflation-adjusted market capitalization greater than $200 million as of most recent year-end. The universe of Large Stocks consists of all securities in the Chicago Research in Security Prices (CRSP) dataset or S&P Compustat Database (or other, as noted) with inflation-adjusted market capitalization greater than the universe average as of most recent year-end. The stocks are equally weighted and generally rebalanced annually.

Hypothetical performance results shown on the preceding pages are backtested and do not represent the performance of any account managed by OSAM, but were achieved by means of the retroactive application of each of the previously referenced models, certain aspects of which may have been designed with the benefit of hindsight.

The hypothetical backtested performance does not represent the results of actual trading using client assets nor decision-making during the period and does not and is not intended to indicate the past performance or future performance of any account or investment strategy managed by OSAM. If actual accounts had been managed throughout the period, ongoing research might have resulted in changes to the strategy which might have altered returns. The performance of any account or investment strategy managed by OSAM will differ from the hypothetical backtested performance results for each factor shown herein for a number of reasons, including without limitation the following:

- Although OSAM may consider from time to time one or more of the factors noted herein in managing any account, it may not consider all or any of such factors. OSAM may (and will) from time to time consider factors in addition to those noted herein in managing any account.

- OSAM may rebalance an account more frequently or less frequently than annually and at times other than presented herein.

- OSAM may from time to time manage an account by using non-quantitative, subjective investment management methodologies in conjunction with the application of factors.

- The hypothetical backtested performance results assume full investment, whereas an account managed by OSAM may have a positive cash position upon rebalance. Had the hypothetical backtested performance results included a positive cash position, the results would have been different and generally would have been lower.

- The hypothetical backtested performance results for each factor do not reflect any transaction costs of buying and selling securities, investment management fees (including without limitation management fees and performance fees), custody and other costs, or taxes – all of which would be incurred by an investor in any account managed by OSAM. If such costs and fees were reflected, the hypothetical backtested performance results would be lower.

- The hypothetical performance does not reflect the reinvestment of dividends and distributions therefrom, interest, capital gains and withholding taxes.

- Accounts managed by OSAM are subject to additions and redemptions of assets under management, which may positively or negatively affect performance depending generally upon the timing of such events in relation to the market’s direction.

- Simulated returns may be dependent on the market and economic conditions that existed during the period. Future market or economic conditions can adversely affect the returns.

The dividend yield is a gross indicated yield. There is no guarantee that the rate of dividend payment will continue and the income derived is subject to taxes and expenses which will impact the actual yield experience of each investor.