Inefficiency Breeds Opportunity in Small Cap Equities

By Chris Meredith, Ehren Stanhope

July 2015

Small cap equities1are generally misunderstood and underappreciated. At O’Shaughnessy Asset Management (OSAM), we believe they present a phenomenal total return opportunity for discerning long-term investors. The construction of common small cap indices and the nuances of the small cap universe favor an active approach. The space has more stocks to choose from but significantly less analyst coverage and lower institutional ownership than larger capitalization ranges. The companies tend to be young and nimble with high growth potential. However, among small cap stocks there is a high degree of variability in quality, valuation, and liquidity that is masked by passive index investments. This paper details the disciplined process and research—accrued over two decades of managing small cap stocks—that we believe can provide small cap investors with consistent long-term total return.

Lack of Coverage & Ownership Drives Inefficiency

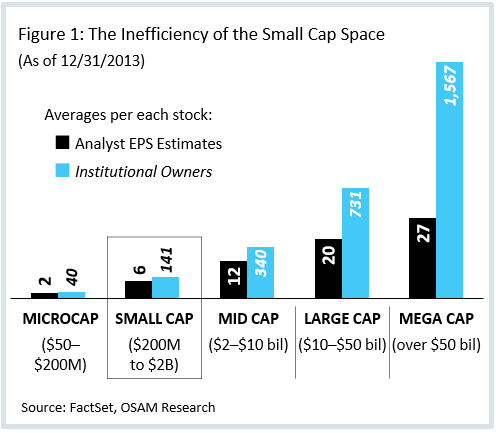

There are currently about three times as many stocks in the small cap space as there are in the large cap space, and ten times the number of mega cap companies. The size of the selection universe presents a significant dilemma for fundamental managers and sell-side analysts. Most fundamental managers, who pride themselves on qualitative analysis of individual companies and management teams, do not have the ability to cover the full breadth of the small cap universe. This is the same scenario for sell-side analysts. The amount of attention the investment community can give to any individual stock is limited. Therefore, focus is shifted toward the largest, most liquid names. As we will demonstrate, the largest, most liquid names tend to be the worst performers. While mega cap stocks have 27 analyst earnings estimates on average, small cap stocks have just six. The small cap average of six is actually skewed high—40 per-cent of the stocks in the small cap space have three or fewer analysts and nearly 20 percent have no analyst coverage at all. Similarly, institutional ownership in small cap tends to be very low. Issues with liquidity and the ability to make investments in size tend to push institutions away from small cap names. The implication is that this lack of coverage and institutional ownership creates significant inefficiency in the space.

Redefine Inefficiency as an Opportunity for Excess Return

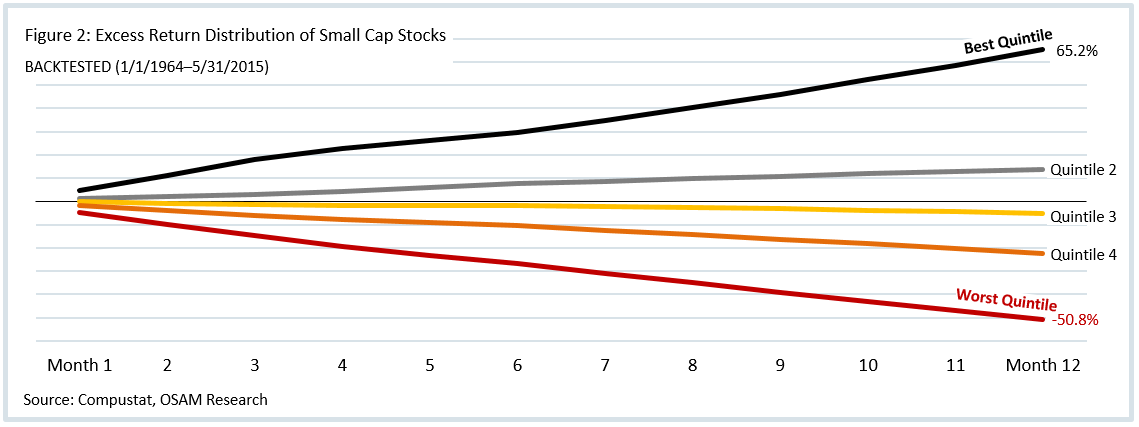

This greater opportunity for total return, born out of inefficiency, is best illustrated by pretending as though we had perfect foresight. We ranked all small cap stocks based on their future return over the next 12 months. The stocks were organized into five buckets (quintiles) from best to worst performance. Keep in mind, this group of stocks is similar to the Russell 2000® Index that has generated an annualized return of 11.5 percent referenced since 1964. The best quintile of stocks outperformed by 65.2 percent per year for more than five decades. On the flip side of the equation, stocks in the worst quintile underperformed by 50.8 percent during the same time period. The wide dispersion suggests there are significant benefits to aligning portfolios with the characteristics of consistent outperformers, while entirely avoiding companies with the characteristics of consistent underperformers. Our research leads us to believe valuation, quality, and momentum are themes that aid us to accomplish these tasks.

Single-Factor Approaches to Valuation are not “Smart”

Value investing works. However, a key consideration is determining what constitutes an undervalued investment. One approach is to allocate to a style index like the Russell 2000® Value. This index tilts stock weights based on price-to-book, earnings growth estimates, and historical sales growth—price-to-book being the dominant factor. The simple application of this tilt allowed the Russell 2000® Value Index to outperform the Russell 2000® Index by 2.2 percent on average back to 1964 with an annualized return of 13.7 percent. The key differentiator for style indices is the application of selection criteria, which is absent in market-cap-weighted indices. But they are still suboptimal because traditional style indices rely on a weak valuation factor (price-to-book) and those indices own companies with poor characteristics, just in lower quantities than market-cap-weighted benchmarks.

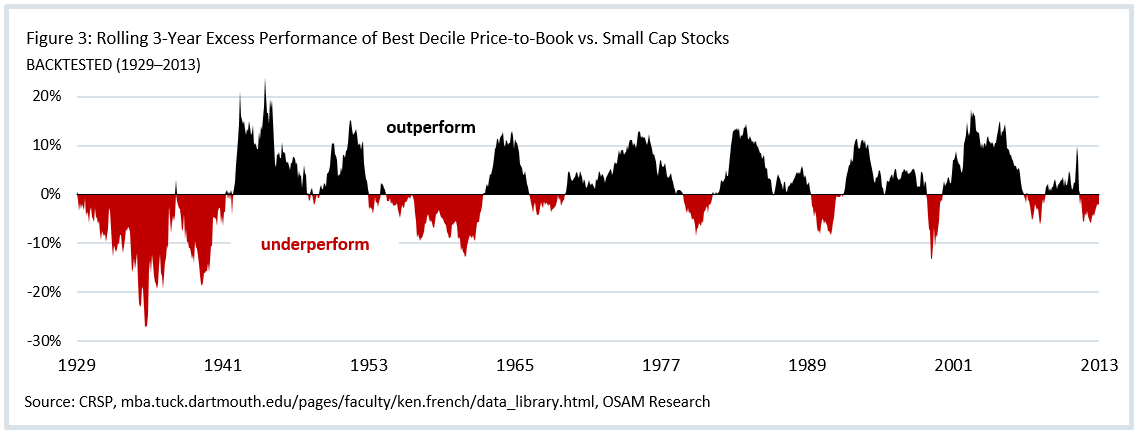

We believe that defining valuation via a single factor is inferior for two reasons. First, just as value and growth styles move in and out of favor, so do individual factors. We evaluate the robustness of factors by testing for consistency over time using base rates. Base rates are batting averages for how often factors outperform the market in rolling periods. Three-year base rates are particularly instructive as that tends to be about the length of time investors are willing to tolerate underperformance. On this measure, price-to-book does not perform well. Investing in the cheapest stocks by price-to-book has merely a 58 percent three-year batting average versus small cap stocks, underperforming in 42 percent of three-year periods—not that impressive. Figure 3 (see next page) is a visual representation of the batting average, showing rolling three-year excess returns of the best decile of price-to-book. There are long periods of time where underperformance tends to be clustered. For 146 months (12.2 years) from 1930 to 1942, the best stocks by price-to-book posted negative excess return over the trailing three-year period, with one exception in January 1938. This happened again from 1955 to 1963 when the best decile of price-to-book posted 96 consecutive months (eight years) of negative three-year excess return.

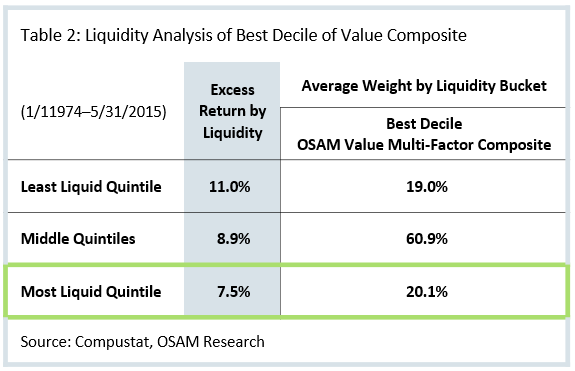

The second reason single factors are inferior to multi-factor composites is that all factors have biases to sectors, cap ranges, and liquidity buckets, which can result in real world implementation issues. Liquidity is a particularly important consideration in the small cap space. If a factor concentrates investments into illiquid stocks, excess return suggested in backtested results may not be realizable in investor portfolios.2 A simple five-million dollar trade in the least liquid quintile of the small cap market can cost upwards of 2.8 percent in terms of market impact—per each trade! Liquidity is critically important in real world implementation.

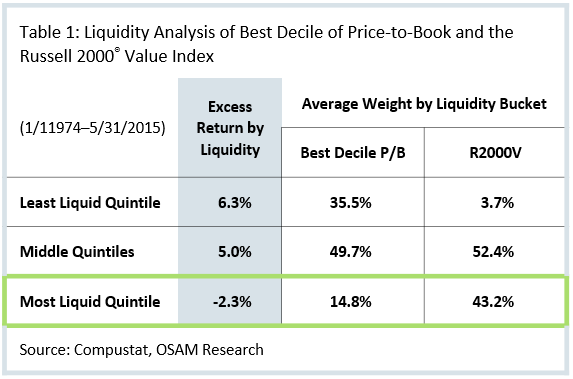

We have found this to be the case with price-to-book. Stocks in the cheapest decile by this factor tend to skew to illiquid names. Currently, the best decile of stocks by price-to-book has a 35-percent allocation to the least liquid names in small cap. It turns out these illiquid names generate the bulk of excess return (+6.3 percent) associated with the factor. The most liquid stocks within the best decile actually underperform by 2.3 percent historically. This is particularly important when thinking about a style benchmark like the Russell 2000® Value Index—43 percent of the index falls into the most liquid quintile, where price-to-book is least effective.

Unbeknownst to most index investors, they are effectively exchanging excess return for greater liquidity and product capacity.

A Multi-Factor Approach is Superior

We believe in the assessment of valuation based on a combination of multiple factors—sales, cash flows, earnings, and return of capital to shareholders—that we refer to as our Value composite. A multi-factor approach provides superior total return, risk-adjusted return, and overall consistency versus numerous single factors that we have tested, including price-to-book.

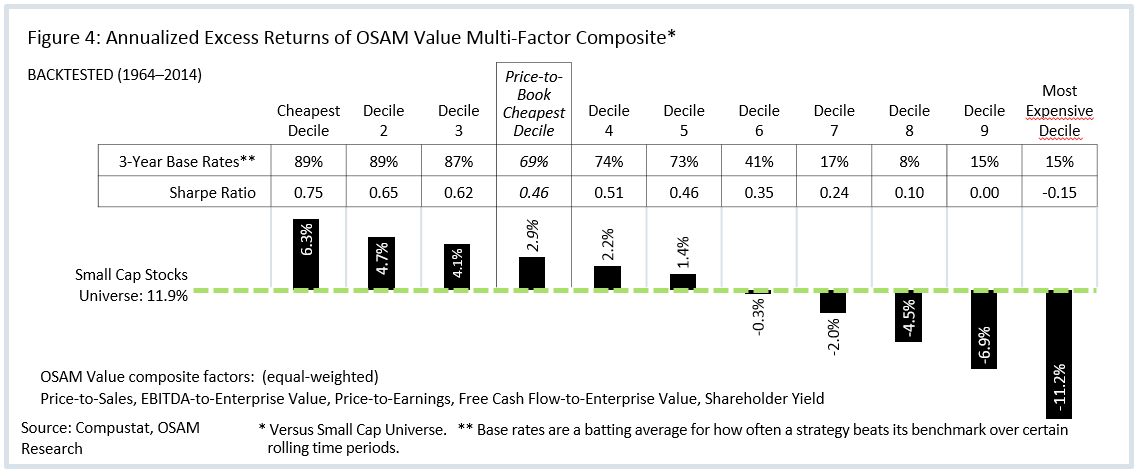

In Figure 4 (see next page), we divide small cap stocks into deciles based on a Value composite score. The least expensive stocks are in the first decile while the most expensive are in the tenth decile. Not only do the most expensive small cap stocks underperform by an astounding 11.2 percent per year from 1964 to 2014, but they do so 85 percent of the time in rolling three-year periods. Invest in these expensive stocks at your own peril. On the other end of the spectrum, the cheapest decile outperforms by 6.3 percent on average while outperforming in 89 percent of all rolling three-year periods.

Diversification and the interactive effects of a multi-factor approach provide more robust results at both ends of the spectrum while also eliminating the aforementioned issue of factor timing. The equal-weighted Value composite outperforms its underlying constituents 83 percent of the time in rolling ten-year periods.

Additionally, multi-factor models tend to mitigate the biases inherent in single factors. Continuing the liquidity analysis, our Value composite is more evenly distributed across liquidity buckets. Unlike price-to-book, the Value composite generates significant and positive excess return in even the most liquid small cap names, which suggests its ability to outperform is not as reliant on illiquidity premiums and the excess returns suggested by researched results are more likely to be realized in a capacity-constrained space.

Avoid Value Traps via a Quality Overlay

Not every cheap stock outperforms. Even within the cheapest decile of value, there is wide dispersion in underlying stock returns. Certain stocks are cheap for a reason: value traps. Small cap stocks exhibit worse quality characteristics on average than their large cap cousins, so quality characteristics play a crucial role in avoiding these traps. Far from esoteric minutiae, the quality characteristics we employ to avoid certain stocks are rooted in key management decision making about how to use shareholder capital, accounting policies, and profitability.

One of the key quality metrics concerns the financing of company operations. Raising capital is commonly viewed as a positive sign because it serves as an indication that a small firm has passed the litmus test of the capital markets. Our research suggests this is a false assumption that is destructive to returns. The quintile of stocks with the greatest debt issuance underperforms by 5.5 percent per year. Companies with the highest share issuance—diluting shareholders—underperform by a greater 6.4 percent per year. The vast majority of small cap stocks engage in these activities. For example, nearly three-quarters of all stocks on the Russell 2000® Index are net diluters of shareholders. Profitability (ROE) and earnings growth tend to be lower overall for small cap companies. Non-cash earnings-to-assets compares the extent to which firms use non-cash accruals to manipulate earnings. There is a tail of companies that do not represent their earnings appropriately.

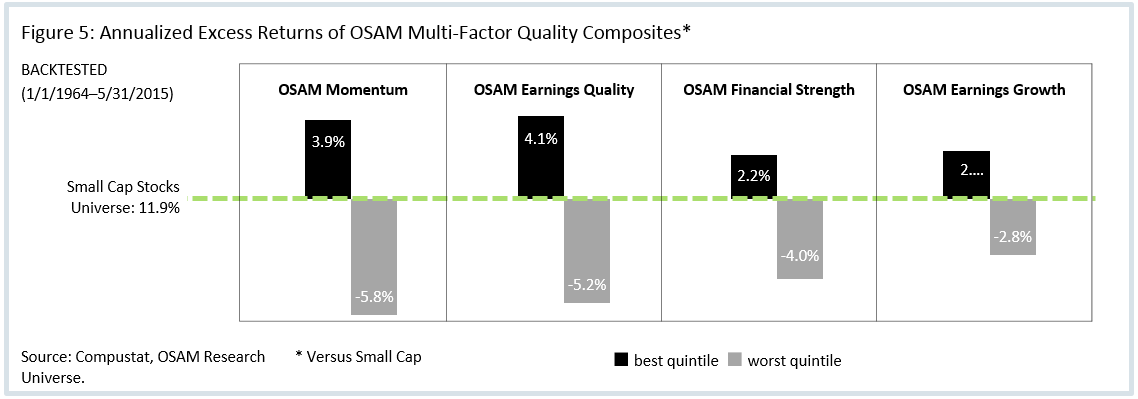

In order to avoid poor quality companies, we remove stocks based on four themes: Financial Strength, Earnings Quality, Earnings Growth, and Momentum. Financial Strength identifies companies that are overly levered, are issuing debt and equity, and have poor cash flow coverage ratios. Earnings Growth assesses profitability and the trend in the growth of earnings. Earnings Quality measures whether earnings are driven by cash generation or non-cash accruals. Momentum looks at the recent market trend over the last three to nine months, as well as the volatility of the stock, and avoids investments that have been penalized heavily and have excessive volatility.

In Figure 5, we evaluate the performance of stocks that fall from highest quality (quintile 1) to lowest quality (quintile 5) according to each theme. In doing so, we generally find that the greatest benefit lies in avoiding the lowest quality stocks. For example, stocks in the worst quintile of Earnings Quality underperform small cap stocks by 5.2 percent per year. With a batting average of just five percent in rolling five-year periods, stocks with the worst Earnings Quality lose to the market 95 percent of the time. We see similar results for Financial Strength and Earnings Growth.

Unite Quality & Valuation in Portfolio Construction

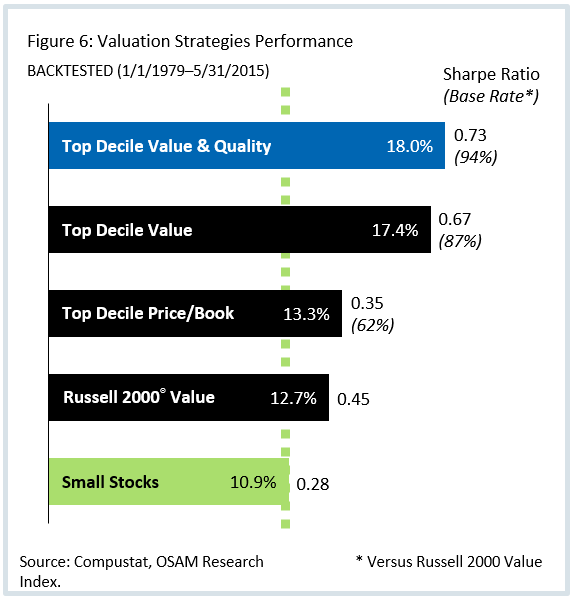

Now that we have individually established the power of valuation for selection and quality for avoidance, we will demonstrate the power of the interactive effects of these themes in portfolio construction. As shown in Figure 6 (see next page), we start with an equal-weighted universe of all stocks with an inflation-adjusted market capitalization between $200 million to $2 billion. To ensure illiquid names are not driving return in our analysis, we eliminate names with less than an inflation-adjusted $250,000 average daily dollar volume. An equal-weighted investment in this small cap universe provides an annualized return of 10.9 percent from 1979–2015. The market-capitalization-weighted Russell 2000® Value Index, which tilts the universe based on price-to-book, provides a greater 12.7 percent annualized return. Focusing further on the top decile of price-to-book yields an improvement in return to 13.3 percent. A significant jump occurs when shifting to the multi-factor Value composite, which returns 17.4 percent.

Finally, we combine the themes of value and quality by first concentrating on stocks in the best decile of the Value composite and then filtering out stocks that rank poorly on quality and momentum. This improves the overall results of the test to an impressive 18.0 percent annualized return. Additionally, the inclusion of quality themes helps lower volatility and risk-adjusted return (Sharpe Ratio). The combination of value and quality also improves the consistency of returns as shown by higher base rates (94%).

CONCLUSION

We have established that poor coverage by institutional owners and analysts drive inefficiencies in the small cap space. This limited attention specifically favors a scalable, disciplined approach, which is able to identify opportunities much more efficiently than traditional qualitative stock picking. Multi-factor valuation based on earnings and cash flows is superior to a simple passive or single-factor investment in small cap stocks based on the book value of equities. The nature of small cap stocks lends itself to poorer overall quality, which requires a discerning view to avoid value traps. Liquidity is an important consideration because it can erode excess returns in real world application. While small cap stocks present a greater opportunity for total return, transaction costs significantly limit the amount of manageable assets in the space. Drawing upon a long history of trading in small caps, we believe that effective trade execution is also a key to successful long-term small cap investing.

While this paper demonstrates the results of our research on a theoretical basis, OSAM has employed a small cap value strategy with similar themes and construction methodology since 2004, which has achieved comparable levels of excess return. O’Shaughnessy Small Cap Value is a live strategy that removes poor names through a combination of Financial Strength, Earnings Quality, Earnings Growth, and Momentum and then selects a concentrated portfolio with the best Value composite scores. This strategy has generated 5.5 percent excess return over the Russell 2000® Value Index since inception, which is in line with the expected outperformance we have seen in our research.

Data Notes:

All factor portfolios cited in this attribution report are calculated using a compositing methodology. Monthly portfolios are created with a 12-month holding period based on a single characteristic within a universe of stocks. The 12 monthly portfolios are then combined together to create the composite portfolio.

The Small Cap Stocks Universe includes all stocks included in the Compustat Database listed on a U.S. exchange with a market value between $200 million and $2 billion, on an inflation adjusted basis, and a price per share greater than $1.

Market Capitalization Ranges are defined follows: Small Cap stocks range from $200 million to $2 billion, Mid Cap from $2 billion to $10 billion, Large Cap stocks greater than $10 billion.

The Russell 2000® Value Index measures the performance of the small cap value segment of the U.S. equity universe. It includes those Russell 2000® companies with lower price-to-book ratios and lower forecasted growth values. The Russell 2000® Index measures the performance of the small-cap segment of the U.S. equity universe. It includes approximately 2,000 of the smallest securities based on a combination of their market cap and current index membership

Footnotes:

1Throughout this paper, we will refer to small cap stocks for all research. This universe includes all stocks trading on the NYSE, AMEX, and NASDAQ with an historical inflation-adjusted market capitalization between $200 million and $2 billion.

Composite Performance Summary

For the full composite performance summary of O’Shaughnessy Small Cap Value, please follow this link: http://www.osam.com/pDf/osam_factsheet_scv.pdf#page=3&view=Fit

General Legal Disclosure/Disclaimer and Backtested Results

The material contained herein is intended as a general market commentary. Opinions expressed herein are solely those of O’Shaughnessy Asset Management, LLC and may differ from those of your broker or investment firm.

It should not be assumed that your account holdings correspond directly to any comparative indices. Individual accounts may experience greater dispersion than the composite level dispersion (which is an asset weighted standard deviation of the accounts in the composite for the full measurement period). This is due a variety of factors, including but not limited to, the fresh start investment approach that OSAM employs and the fact that each account has its own customized re-balance frequency. Over time, dispersion should stabilize and track more closely to the composite level dispersion. Gross of fee performance computations are reflected prior to OSAM’s investment advisory fee (as described in OSAM’s written disclosure statement), the application of which will have the effect of decreasing the composite performance results (for example: an advisory fee of 1% compounded over a 10 year period would reduce a 10% return to an 8.9% annual return). Portfolios are managed to a target weight of 3% cash. Account information has been compiled by OSAM derived from information provided by the portfolio account systems maintained by the account custodian(s), and has not been independently verified. In calculating historical asset class performance, OSAM has relied upon information provided by the account custodian or other sources which OSAM believes to be reliable. OSAM maintains information supporting the performance results in accordance with regulatory requirements. Please remember that different types of investments involve varying degrees of risk, that past performance is no guarantee of future results, and there can be no assurance that any specific investment or investment strategy (including the investments purchased and/or investment strategies devised and/or implemented by OSAM) will be either suitable or profitable for a prospective client’s portfolio. OSAM is a registered investment adviser with the SEC and a copy of our current written disclosure statement discussing our advisory services and fees continues to remain available for your review upon request.

Hypothetical performance results shown on the preceding pages are backtested and do not represent the performance of any account managed by OSAM, but were achieved by means of the retroactive application of each of the previously referenced models, certain aspects of which may have been designed with the benefit of hindsight.

The hypothetical backtested performance does not represent the results of actual trading using client assets nor decision-making during the period and does not and is not intended to indicate the past performance or future performance of any account or investment strategy managed by OSAM. If actual accounts had been managed throughout the period, ongoing research might have resulted in changes to the strategy which might have altered returns. The performance of any account or investment strategy managed by OSAM will differ from the hypothetical backtested performance results for each factor shown herein for a number of reasons, including without limitation the following:

- Although OSAM may consider from time to time one or more of the factors noted herein in managing any account, it may not consider all or any of such factors. OSAM may (and will) from time to time consider factors in addition to those noted herein in managing any account.

- OSAM may rebalance an account more frequently or less frequently than annually and at times other than presented herein.

- OSAM may from time to time manage an account by using non-quantitative, subjective investment management methodologies in conjunction with the application of factors.

- The hypothetical backtested performance results assume full investment, whereas an account managed by OSAM may have a positive cash position upon rebalance. Had the hypothetical backtested performance results included a positive cash position, the results would have been different and generally would have been lower.

- The hypothetical backtested performance results for each factor do not reflect any transaction costs of buying and selling securities, investment management fees (including without limitation management fees and performance fees), custody and other costs, or taxes – all of which would be incurred by an investor in any account managed by OSAM. If such costs and fees were reflected, the hypothetical backtested performance results would be lower.

- The hypothetical performance does not reflect the reinvestment of dividends and distributions therefrom, interest, capital gains and withholding taxes.

- Accounts managed by OSAM are subject to additions and redemptions of assets under management, which may positively or negatively affect performance depending generally upon the timing of such events in relation to the market’s direction.

- Simulated returns may be dependent on the market and economic conditions that existed during the period. Future market or economic conditions can adversely affect the returns.