Custom Indexing: The Next Evolution of Index Investing

By Patrick O’Shaughnessy

December 2020

By 2025, most financial advisors will use web-based software to create and manage Custom Indexes for their clients. Standard indexes have a single methodology; one ruleset dictating what they own and how they rebalance. Standard indexes are “one size fits all.” Like standard indexes, Custom Indexes also invest and rebalance according to a defined methodology. But with Custom Indexes, the methodology is personalized based on an investor’s circumstances and preferences and can be easily adjusted as an investor’s circumstances change. This flexibility is possible because Custom Indexes are implemented through separate accounts, where investors can directly own a custom mix of individual stocks and bonds rather than indirectly owning positions through a collection of funds and ETFs.

Custom Indexing is a technology, and technology often removes barriers. Co-mingled funds and ETFs sit in between investors and the stocks they own. Funds and ETFs have been good to investors and were wonderful technologies in their own rights. But Custom Indexing software, zero commission trading, and fractional share trading mean that in the future, more investors will own their shares directly rather than through mutual funds and ETFs.

If what we’ve seen with Canvas (O’Shaughnessy Asset Management’s Custom Indexing platform, now one year old) is any indication of the future, Custom Indexes will be built using dynamic software, typically starting with broad market exposure (i.e. beta) and then accounting for each investor’s needs in areas like taxes and tax treatment, desired returns, income, risk exposures, ESG, and more.

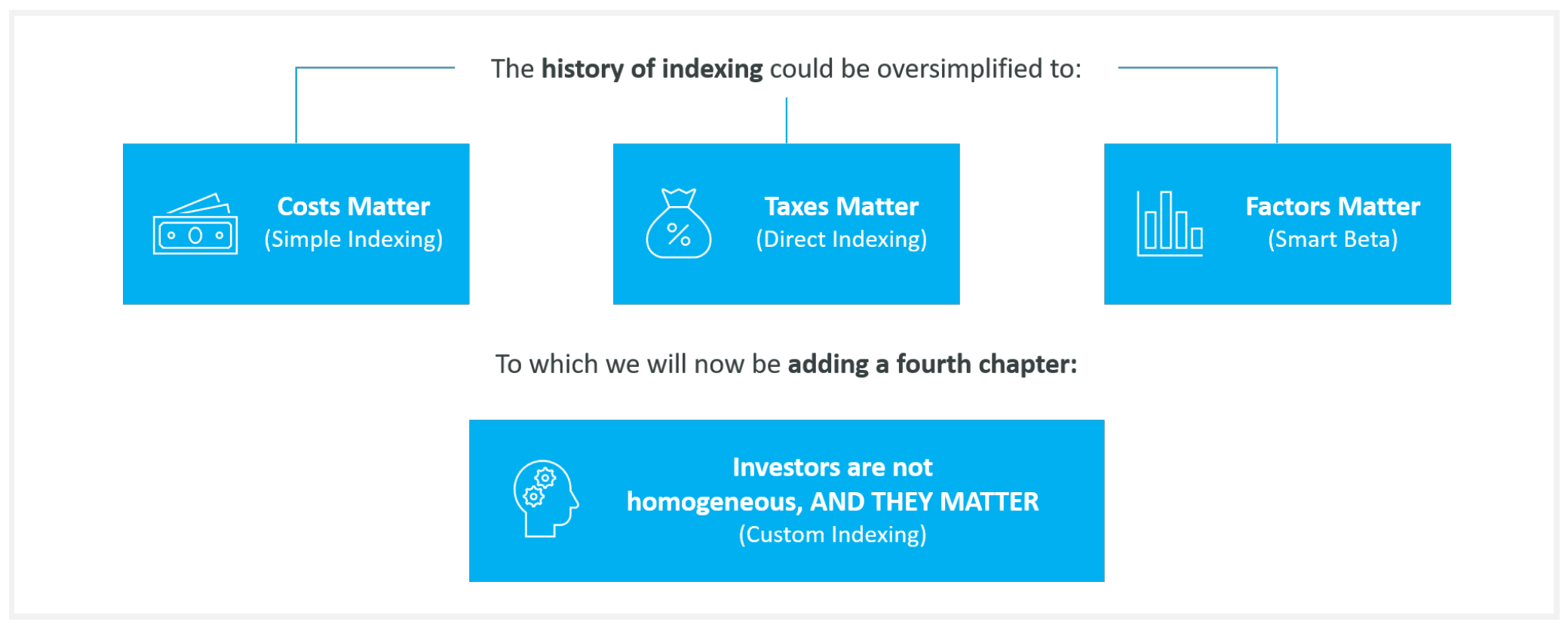

Custom Indexing will win significant share from simple indexing and Direct Indexing because it will continue to offer the benefits of its predecessors (low cost and tax friendly) while layering in significant new benefits.

An Inevitable Future

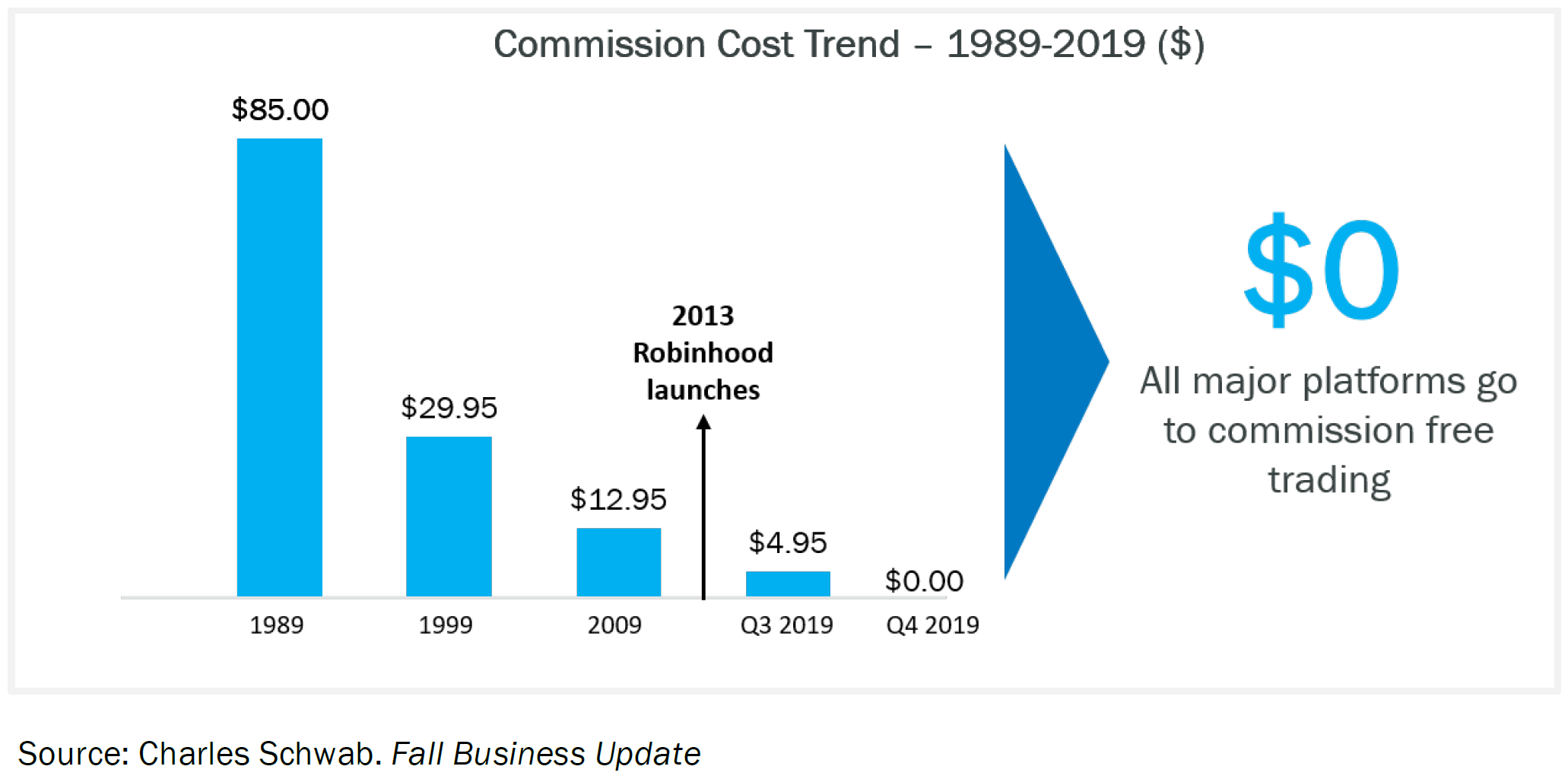

Custom Indexing is a great example of a new product which sits on what my friend Josh Wolfe calls a “directional arrow of progress.” In technology, we can observe trend lines, arrows of progress, that show improvement in key product dimensions that matter to customers (often cost, speed, convenience, selection, and personalization). Because technology tends to advance consistently (and often, exponentially), it’s often safe to extrapolate these technology-based trends into the future. A simple example in the world of investing is the cost (commission) of a single-stock trade for retail investors. Costs marched steadily downwards until Robinhood jumped the line and brought them to zero. The other major brokerage platforms had to follow suit.

When we launched OSAM in 2007, we began ripping out third-party software and technology solutions because they did not meet our needs. We slowly built our own software and research-technology stack piece by piece. This build out put us in a unique position to develop the first Custom Indexing platform, as we were able to build it on top of the software infrastructure we’d laid previously. Because we were first to this new market with Canvas, we’ve seen the future of how Custom Indexing will work:

Each advisory firm that we’ve worked with started by making their own set of Custom Index strategy templates which reflect their firm’s investing views (see summary box on pg 4 for template examples). You can think of these like a basic set of blueprints which a home builder uses repeatedly before tweaking each home to the needs and tastes of the homeowner. Each firms’ templates are different than the others, which highlights the power of a fully customizable platform. After building their strategy templates, our advisor firms have further tailored strategy rules at the individual account level based on specific client circumstances and preferences.

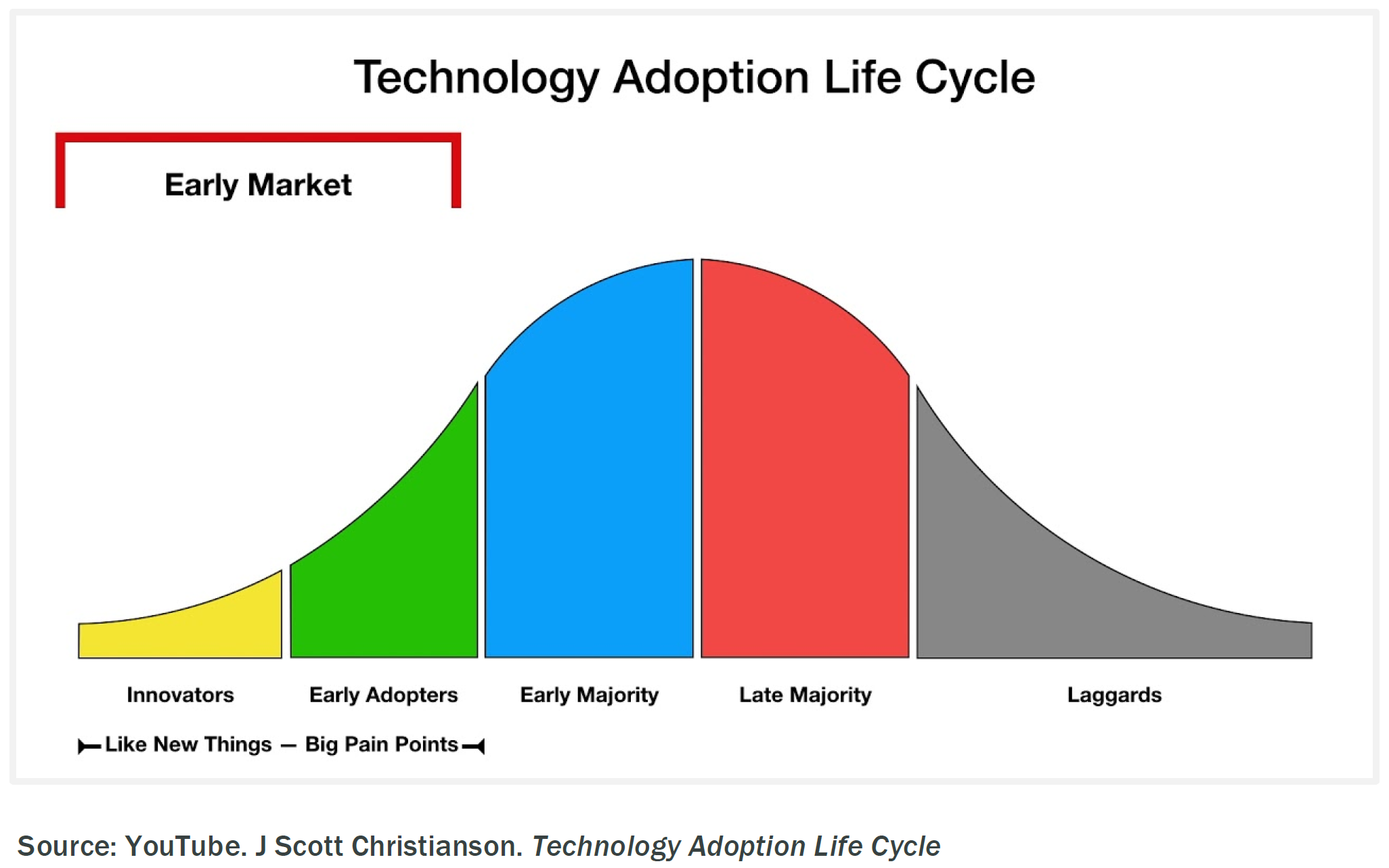

Today, when you extrapolate the trend lines in portfolio management, the natural conclusion for where we are heading is Custom Indexing. We are seeing the most advanced RIAs begin to consider and adopt Custom Indexing solutions. In the commonly used “technology adoption curve” shown below, the “innovators” have started using Custom Indexes. Soon, we’ll begin working with “early adopters.” But before too long, some advisors will be playing catch up, as the ability to build a customized strategy will be table stakes for winning new clients and continuing to improve relationships with existing clients.

I often find it helpful to squint and look out five to ten years, rather than focusing on the next year or two. This makes certain things easier to predict. In this case, can anyone imagine a world where Custom Indexing doesn’t dominate? I find it very hard to imagine because most of the frictions that would have stopped Custom Indexing as a practice – mostly in the form of dollar costs and manual workflows – have already disappeared. Because we believe this is an inevitability, we believe that the top advisors should be thinking about how they will embrace this new technology now.

How We Got Here

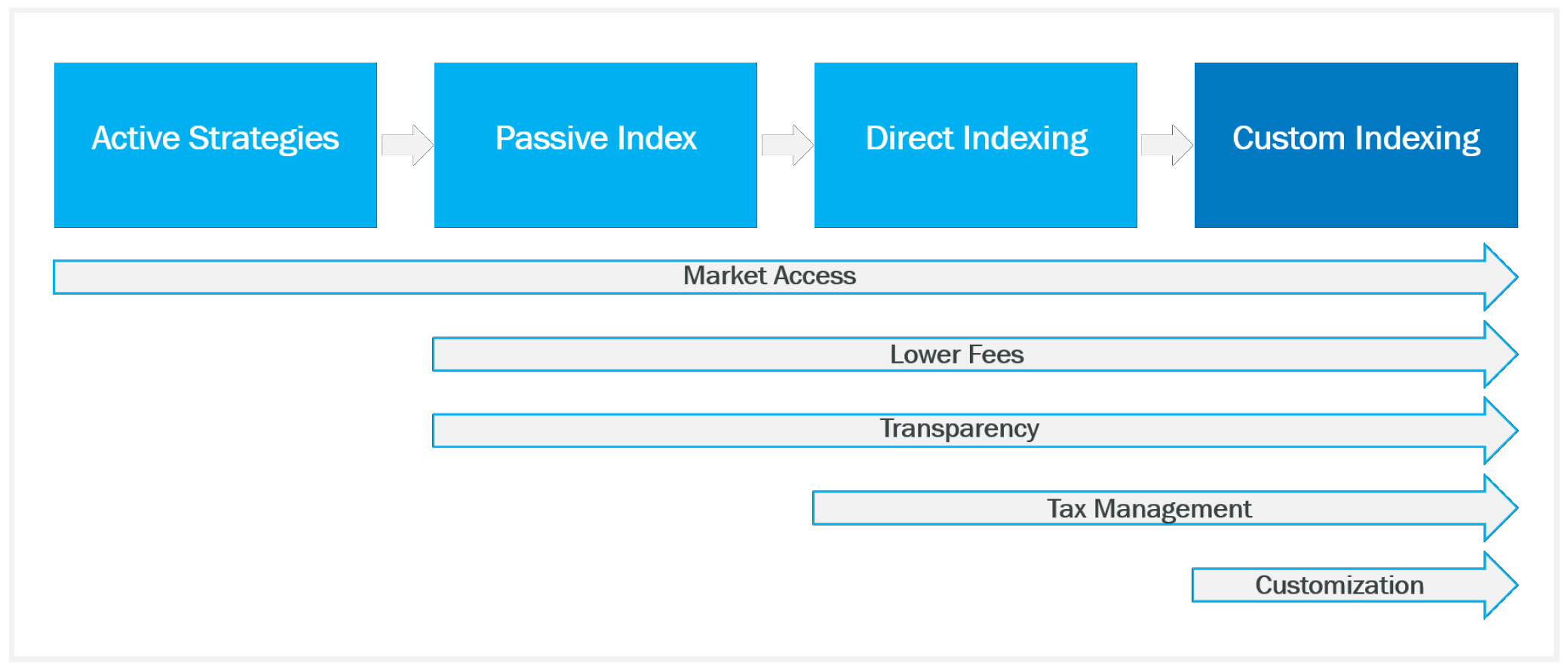

Each simple step in the indexing progression builds on the last. Direct Indexing carried forward the low-cost benefits of simple indexing, and Custom Indexing will carry forward the benefits of low costs and tax-loss harvesting.

Once advisors adopt a Custom Indexing solution, they will not go backwards to funds because there will be no reason to trade down for less overall functionality. Even for those who have a client that wants to only own the S&P 500 with no modifications in a non-taxable account, a Custom Indexing platform will be able to fulfill that need as well as a simple index firm could, again thanks to increasingly sophisticated technology.

Why Now

So why haven’t Custom Indexes and Custom Indexing platforms appeared until now? Because the software required is hard to build and industry conditions—including zero commission trading—are only now evolved enough to make it possible. We built Canvas on top of a decade’s worth of custom-built internal software. Our inspiration was Amazon Web Services’ strategy of offering their internal tools as external services. We’ve essentially done the same thing with Canvas, but it took us 10 years to build and refine those tools (in the areas of trading, performance, daily model generation and rebalancing, and account management). These systems, with internal names like Workbench and Trade Builder, are the lifeblood of OSAM’s separate account business.

Thanks to this pre-existing software infrastructure and our existing team, we were lucky to be the first offering in this new category when we launched Canvas in late 2019. We fully expect more entrants to begin to offer Custom Indexing platforms in the coming years.

What We’ve Learned

Following the advice of Chetan Puttagunta at Benchmark Capital, we decided to recruit a small group of original partners at launch and stick with them, building what they need, for a long period of time after launch. Chetan said this process would take 1 to 3 years, which made me scoff at first. Yet, here we are a year later, having learned a tremendous amount and having built a more complete system. Chetan was right that building a platform like this requires patience and care.

Now that we are managing nearly 500 accounts and are nearing $1B of assets on Canvas, we have learned several key things about Custom Indexing that we didn’t know when we started:

1. Customization does matter

70% of our ~500 accounts have totally unique settings. We’d expect that percentage to rise as advisors continue to get comfortable with this new way of managing their clients’ money.

2. Taxes are central

Since we first launched, our customers have pushed us to build more nuanced and useful custom-tax features into the platform. Direct Indexing improved simple indexing for taxable investors by generating useful tax losses while sticking close (enough) to the performance of the simple index. What we’ve learned is that tax losses are important, but so is customization around one’s tax strategy.

Investors and their advisors wanted to be able to customize:

- The maximum amount of taxable gains realized while trading their portfolio (in both dollar and percentage terms)

- The tax budget when transitioning from their old portfolio to their new Custom Index

- The tracking error allowed to generate tax losses (sometimes moved higher in years when there are lots of gains to offset, sometimes lower to stick closer to their underlying Custom Index strategy)

Each of these required a large software build to manage but are among the more used features for advisors with their clients (which fits in nicely with the complex tax planning they are often doing for their clients already).

3. Factor exposures are a means, not an end

Our history is one of factor-based investing. We’ve spent our collective careers defining factors in as much detail as possible, typically seeking the best absolute or risk-adjusted excess return as we build our models.

But Canvas has taught us that often investors are seeking something other than purely returns.

We’ve learned that risk, income, downside protection, or exposure to innovative companies are also key outcomes that people want to achieve, and they want to use factor-based strategies to achieve those outcomes.

Factors are simply tools to improve the probabilities of certain outcomes that investors care about. Based on investor demand, we have started offering new strategies focused on stability and income. In the future, we expect Canvas will offer a wide range of quantitative factor building blocks that can be arranged to target specific outcomes.

4. ESG is personal

For years, ESG had a lot more bark than bite. It seemed to survive as a topic just as fodder for industry panels and was rarely actually implemented in client portfolios. We can see this shifting as I write. More investors are wanting some sort of consideration of ESG factors in their portfolios, but here again, we’ve learned that ESG means something unique to most investors. Some investors care exclusively about the elimination of fossil fuels. Others seek to avoid companies which produce unhealthy consumer products. And others want to adjust their portfolio for a whole wide range of issues important to them and their families.

So here again, we find the need for customization. We’ve encountered many investors unhappy with ETF-based ESG offerings which often do too many things at once for investors. They end up not solving the specific issues that investors want to control for in their portfolios. They also tend to focus on avoiding stocks with bad scores, whereas Custom Indexing includes avoiding and tilting towards (giving higher portfolio weight to) companies with the best scores.

We don’t have a strong view as a firm that these factors will do much to returns in a portfolio. All we know is that the stricter the ESG settings, the higher the tracking error tends to be in the portfolio. But for many, that is a fine and a fair trade-off.

5. Custom Indexes require custom reporting

One of the largest barriers to making Custom Indexing work for advisors is ongoing client reporting. After all, if each investor has their own unique strategy, they’ll have their own unique performance (to some degree1). Traditionally, most advisors have their investors in the same few strategies, so reporting becomes a one-size fits all exercise. Custom Indexing changes that, and we’ve spent more time building a new custom reporting engine than on any other project. I suspect in five years, this will all be incredibly sleek, fast, and delivered directly to the end customer via personalized mobile and web applications.

6. The competitive battlefields in Custom Indexing will be quantitative research and software development

The most unique aspect of building a Custom Indexing platform is that it requires two R&D teams. First, the quantitative investment research team and second, the software development team. These two groups must work in close connection but do largely independent work. I’ve said since day one of my tenure running OSAM that the future of our business lies at the intersection of research and technology. Now, I know this is true.

For Custom Indexing to work for advisors, it needs to all live in web-based software that gives advisors a simple, intuitive, user interface. Advisors need to be able to build, track, and report on client Custom Index strategies all in one place. They need to be able to easily create investment templates that address their unique firm philosophy, but then address each of their clients’ unique objectives (with scale in mind). This means that Custom Index providers need to be experienced asset management firms that have technology at their core.

Where We Go from Here

Custom Indexing may be inevitable on a 5-10 year timeline, but we all live in the here and now. We focus on problems directly in front of us, not those around the corner. For RIAs, switching to a new foundational platform is a large and time intensive choice. But we believe those who jump the line and adopt a Custom Indexing approach now, will have a significant competitive advantage with clients and prospects. Custom Indexing naturally comes with supporting software tools for reporting and other tasks that used to require manual work. So, these new software platforms will help free up time for advisors to focus on what matters most – meeting new clients and doing more for existing clients.

As for OSAM, we believe in this directional arrow of progress in portfolio management. We will continue to try to “jump the line” in as many areas as we can. Index investing has always been formulaic. The formula for the first index fund was: buy all listed stocks, weighted by their float-adjusted market cap. Today, there are thousands of strategies based on quantitative formulas that give investors exposure to themes, factors, or other categories, made available through funds, ETFs, and sometimes separate accounts. But in the future, investors will no longer buy into someone else’s formula: each investor will buy into their own.

1 While customization does alter performance, we’ve found most advisors adopt a firm level baseline

GENERAL LEGAL DISCLOSURES & HYPOTHETICAL AND/OR BACKTESTED RESULTS DISCLAIMER

The material contained herein is intended as a general market commentary. Opinions expressed herein are solely those of O’Shaughnessy Asset Management, LLC and may differ from those of your broker or investment firm.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by O’Shaughnessy Asset Management, LLC), or any non-investment related content, made reference to directly or indirectly in this piece will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this piece serves as the receipt of, or as a substitute for, personalized investment advice from O’Shaughnessy Asset Management, LLC. Any individual account performance information reflects the reinvestment of dividends (to the extent applicable), and is net of applicable transaction fees, O’Shaughnessy Asset Management, LLC’s investment management fee (if debited directly from the account), and any other related account expenses. Account information has been compiled solely by O’Shaughnessy Asset Management, LLC, has not been independently verified, and does not reflect the impact of taxes on non-qualified accounts. In preparing this report, O’Shaughnessy Asset Management, LLC has relied upon information provided by the account custodian. Please defer to formal tax documents received from the account custodian for cost basis and tax reporting purposes. Please remember to contact O’Shaughnessy Asset Management, LLC, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you want to impose, add, or modify any reasonable restrictions to our investment advisory services. Please Note: Unless you advise, in writing, to the contrary, we will assume that there are no restrictions on our services, other than to manage the account in accordance with your designated investment objective. Please Also Note: Please compare this statement with account statements received from the account custodian. The account custodian does not verify the accuracy of the advisory fee calculation. Please advise us if you have not been receiving monthly statements from the account custodian. Historical performance results for investment indices and/or categories have been provided for general comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your account holdings correspond directly to any comparative indices. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. O’Shaughnessy Asset Management, LLC is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice. A copy of the O’Shaughnessy Asset Management, LLC’s current written disclosure statement discussing our advisory services and fees is available upon request

The risk-free rate used in the calculation of Sortino, Sharpe, and Treynor ratios is 5%, consistently applied across time

The universe of All Stocks consists of all securities in the Chicago Research in Security Prices (CRSP) dataset or S&P Compustat Database (or other, as noted) with inflation-adjusted market capitalization greater than $200 million as of most recent year-end. The universe of Large Stocks consists of all securities in the Chicago Research in Security Prices (CRSP) dataset or S&P Compustat Database (or other, as noted) with inflation-adjusted market capitalization greater than the universe average as of most recent year-end. The stocks are equally weighted and generally rebalanced annually

Hypothetical performance results shown on the preceding pages are backtested and do not represent the performance of any account managed by OSAM, but were achieved by means of the retroactive application of each of the previously referenced models, certain aspects of which may have been designed with the benefit of hindsight

The hypothetical backtested performance does not represent the results of actual trading using client assets nor decision-making during the period and does not and is not intended to indicate the past performance or future performance of any account or investment strategy managed by OSAM. If actual accounts had been managed throughout the period, ongoing research might have resulted in changes to the strategy which might have altered returns. The performance of any account or investment strategy managed by OSAM will differ from the hypothetical backtested performance results for each factor shown herein for a number of reasons, including without limitation the following:

- Although OSAM may consider from time to time one or more of the factors noted herein in managing any account, it may not consider all or any of such factors. OSAM may (and will) from time to time consider factors in addition to those noted herein in managing any account.

- OSAM may rebalance an account more frequently or less frequently than annually and at times other than presented herein.

- OSAM may from time to time manage an account by using non-quantitative, subjective investment management methodologies in conjunction with the application of factors.

- The hypothetical backtested performance results assume full investment, whereas an account managed by OSAM may have a positive cash position upon rebalance. Had the hypothetical backtested performance results included a positive cash position, the results would have been different and generally would have been lower.

- The hypothetical backtested performance results for each factor do not reflect any transaction costs of buying and selling securities, investment management fees (including without limitation management fees and performance fees), custody and other costs, or taxes – all of which would be incurred by an investor in any account managed by OSAM. If such costs and fees were reflected, the hypothetical backtested performance results would be lower.

- The hypothetical performance does not reflect the reinvestment of dividends and distributions therefrom, interest, capital gains and withholding taxes.

- Accounts managed by OSAM are subject to additions and redemptions of assets under management, which may positively or negatively affect performance depending generally upon the timing of such events in relation to the market’s direction.

- Simulated returns may be dependent on the market and economic conditions that existed during the period. Future market or economic conditions can adversely affect the returns.