An Ancient Relationship: FinTech and Financial Advice

By Jamie Catherwood

May 2019

Watch as Jamie Catherwood discusses this article on Bloomberg

Few modern professions have lasted as long as the financial adviser, which archaeological evidence in Mesopotamia dates to at least the third millennium BCE. From this period, excavators have unearthed a clay tablet documenting the calculations of an ancient financial planning tool. Now, some five thousand years later, there are 12,578 SEC-registered investment advisers (RIAs) managing $82.5T in assets, a figure that has increased $33.1 trillion in the last seven years alone.

How has this profession lasted so long? The industry’s longevity is largely attributable to financial technology (FinTech), which has historically empowered advisers to better serve their clients. Many companies, for example, offer advisers quantitative and accurate measurement of investors’ risk tolerance. Equipped with this technology, advisers have a better sense of how clients will respond to volatility, and can construct portfolios that most accurately reflect a client’s ability to endure market swings.

Humans have always needed help managing their finances and they will for the foreseeable future. As the financial investing ecosystem has evolved, so too have the tools available to financial intermediaries. For while the technology is constantly changing, the industry is everlasting.

The best advisers are those who embrace the most helpful new tools to help them better serve their clients.

Ancient FinTech

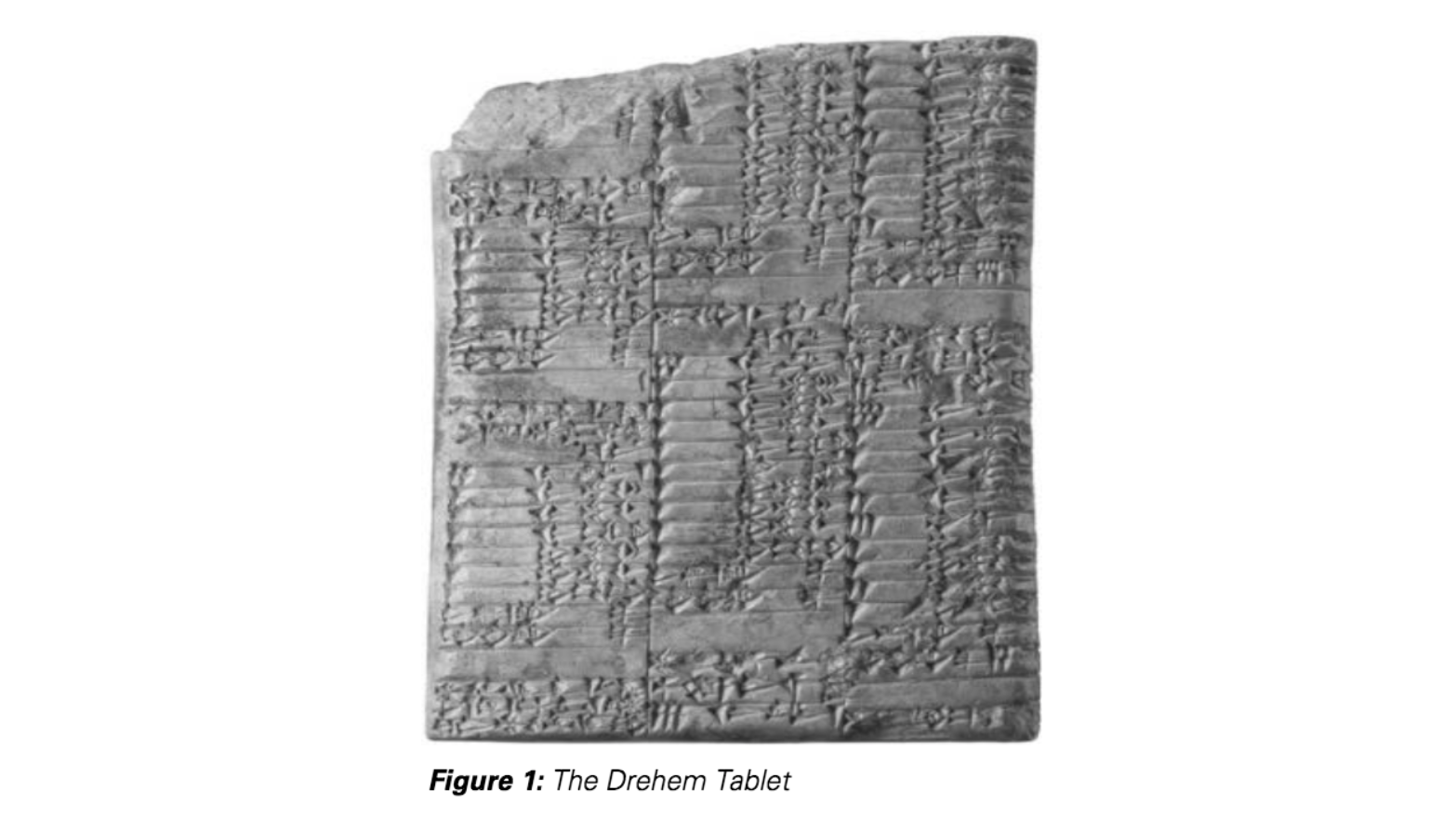

“A cuneiform document from a slightly later period in the third millennium BCE demonstrates not only the importance of raising livestock as big business, but also the extraordinary level of mathematical sophistication it required… it represents a key development in the software of finance. It is a mathematical model of growth used to formulate a long-term financial plan.”

– William N. Goetzmann1

In the modern era, advances within data analytics and software programming have led to a booming market for financial technology products. The underlying driver of everything, however, is computer code. Without coding, there is no modern FinTech. Today we have Python, but in Ancient Mesopotamia, the platforms and tools were powered by Cuneiform, the original coding language.

One of the first known examples of a cuneiform powered platform is the ‘Drehem tablet’, circa 2100 BCE. The technology was an early financial planning tool used for calculating the future value of a client’s assets. In this case, the assets were cows, and the tool forecasted the herd’s growth over a decade, as well as its estimated output of milk and cheese. Even more impressive, this milk and cheese ‘dairy yield’ was measured in Drehem’s local currency, silver.2

These days advisers don’t generally concern themselves with the economic value of a herd’s dairy production, but variations of the underlying financial planning technology still exist.

Substituting a client’s portfolio of stocks and bonds for the herd of cattle, and dividends/interest in place of milk/cheese, this is the same software used by advisors today.

However, some problems have persisted for five thousand years as well, including overly optimistic return assumptions. For example, according to the Drehem model, no member of the herd would ever die, and every mated pair of cows would produce a calf each year.3 This scenario was unrealistic, to say the least. It was akin to an adviser assuming their client’s portfolio would return 10% every year, and never experience a market downturn.

Enabled by Cuneiform ‘coding’, the Drehem tablet offers an early example of FinTech empowering financial advisers. Access to this technology enabled more customizable calculations for clients by allowing advisers to adjust the model’s inputs (herd size, dairy prices, grain prices, currency value, time horizon), which led to more personalized advice.

* * *

This use of technology platforms for offering financial advice persisted over the ensuing centuries, with the bankers of Ancient Athens offering a prime example. The terminology in Athenian finance was a testament to the importance of platforms for advisers in itself. The Greek word for banks, trapeza, referred to the physical table, or ‘platform’, on which bankers operated their business.

Yale Professor William Goetzmann points out that “the names of the earliest banks referred to the medium through which the activity occurred rather than its location”.4

Building upon the technological foundations in Drehem, the Salamis tablet was an equally invaluable tool for Athenian bankers because of the advanced instruments ‘installed’ on the platform. Various sliders and measuring tools were engraved in the stone slab that enabled financiers to make customizable calculations.5

Evidenced by the Salamis and Drehem tablets, the concept of operating a ‘platform’ with financial tools powered by coding ‘languages’ was here to stay.

The Gilded Age: Telegraphs, Tickers, and Technology

"Yankee ingenuity devised an instrument called the 'ticker', which automatically prints abbreviated names of stocks… and the speed with which they are collected and published is a marvel. The quotations are obtained by employees of the Exchange… [and] are immediately reported to telegraph offices on the floor. They are disseminated instantly… [and] American dealers hover over, and intently watch the 'ticker' as it rapidly unwinds the tangled web of financial fate."6

- George Rutledge Gibson (1889)

In addition to improving the accuracy of information and financial advice, technology has historically served as a means for democratizing access to market data. The introduction of the stock ticker in 1867 was a pivotal moment in the history of financial technology. In fact, some historians laud “the stock ticker as the first technology specifically designed to financial markets”.7 In order to fully appreciate its impact on financial markets, however, we must understand how they functioned previously.

* * *

In the 21st Century, where anyone with a smart phone or computer can obtain real-time market data with just a few clicks, the quality of information available to investors in the 19th century is shocking.

For starters, investors received quotations at an abysmally slow pace. The large brokerage firms like Richard Irvine & Co. were known to provide stock prices that were twelve days old, and major publications like the Wall Street Journal only began publishing closing prices in 1868.8 Even when these prices were published, however, it was not necessarily beneficial to investors, since there was no standardized system in place:

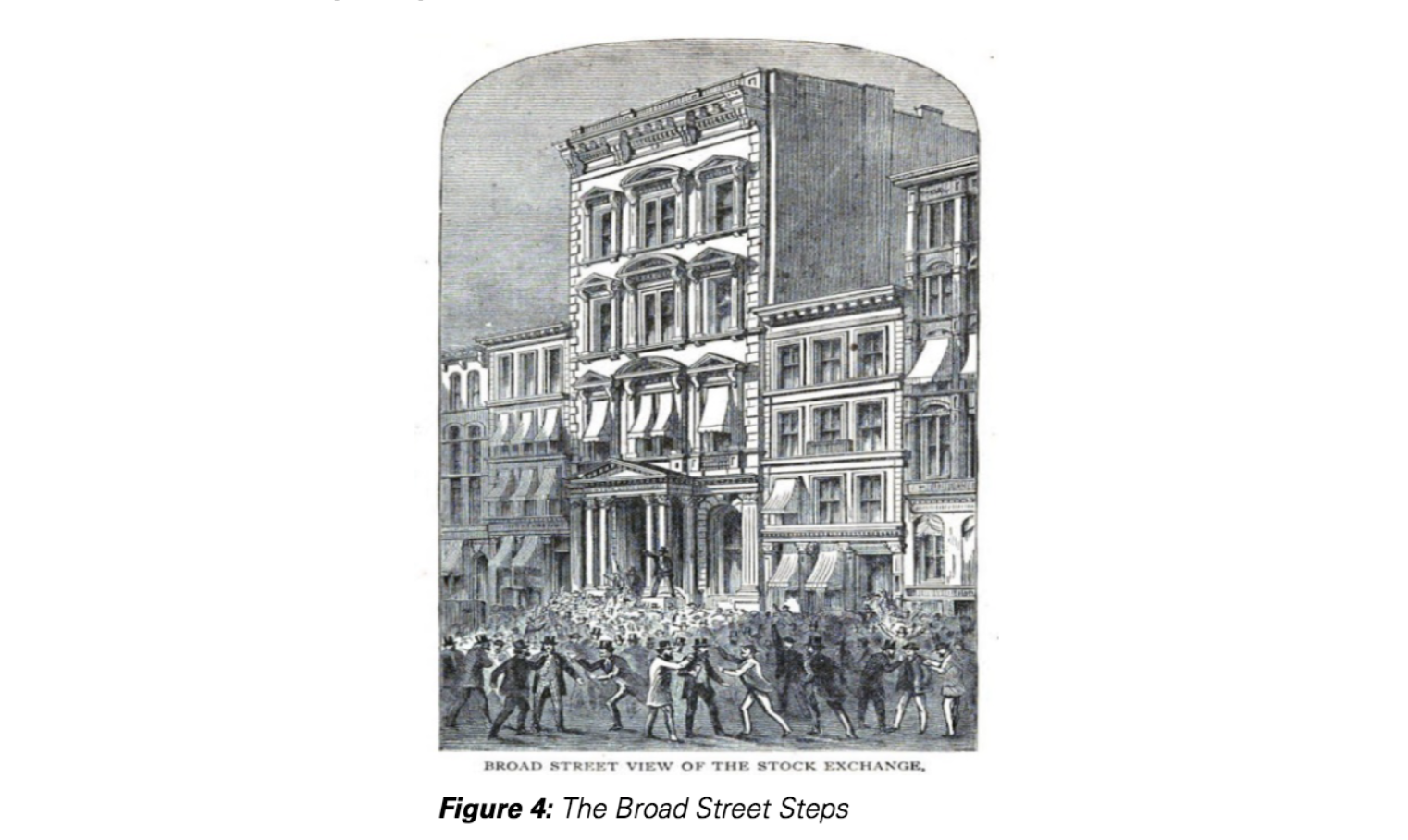

“The room was closed at 5 P.M., after which hour the members were accustomed to gather on the Broad Street steps and continue the dealings till dark. There were no official closing quotations. The newspapers would publish such late quotations as some broker, who remained late, saw fit to furnish.”9

- Francis Eames (1894)

Trusting the accuracy and credibility of the last broker trading each day was unreliable, since brokers often held ulterior motives and reported the closing prices as higher/lower than they really were. Under this system, forgery, typing errors, and manipulation were rampant.

With each added layer of communication between the data source (the exchange) and end investor in the pre-ticker era, the accuracy of information worsened.

* * *

It was in this environment of ridiculously delayed, and often inaccurate information, that Edward Calahan invented his revolutionary technology:

“Mr. Calahan had noticed the congestion of business around the halls of the Stock Exchange, which was largely caused by the brokers and their clerks struggling to secure the latest quotations... These were recorded on suitable pads and then carried by hand to the various Wall Street offices. Active brokers and their messengers were at that time often called ‘pad shovers,’… It occurred to Mr. Calahan that an instrument might be constructed which would record automatically the names of securities and the figures representing quotations or selling prices.”10

- Horace L. Hotchkiss (1905)

His invention was arguably the most important FinTech ever produced, as it provided a visualization of the market for investors of any size or background, and acted as a literal “recorded history of the market”.11

The ticker technology served as a means for democratizing access to market information. Prior to its invention, only those physically present at the stock exchange - or very close by - were privy to real-time market prices. Everyone else received their data at a substantial lag, often to the point where it was no longer useful. Once the ticker was released, however, cables and telegraphs connected brokers across the country to a network of data constantly flowing from a central source, the New York Stock Exchange. According to Horace Hotchkiss, 23,000 offices paid for ticker services in the United States.12

“Many brokers lease wires to connect their Wall Street offices with branches in other parts of the city and country… Another firm paid last winter a large sum for a private wire connecting with a branch at Palm Beach… The transactions and prices of one market are, by its use, now known simultaneously… Distance and time have been annihilated.”13

* * *

In addition to democratizing access, the ticker standardized market information. The thousands of broker offices utilizing this new financial technology received the same data, from the same source.

For investment advisers, the ticker FinTech was a godsend. Far from disrupting their industry, the new technology sparked a demand for their services like never before. With so much data and information suddenly available, people increasingly required investment guidance. One investor lamented in 1908:

"’The trouble with the investment business is,’ he continued, ‘there is no recognized authority. Every house has its own axe to grind and there is no individual of prominence to whom an investor may go for an unbiased opinion and be sure of getting it… if you contemplate the purchase of a building there are appraisers whose services are available;

But this buying a bond because the house having it for sale recommends it, seems to me like going to the manufacturer of Carter's Little Liver Pills and asking, 'What's good for the liver?' You cannot expect him to recommend Warner's Safe Cure nor Pale Pills for Pink People, although he may know in his heart that the pale kind are just what you need.’;

‘Take the medical profession… ‘When you are ill you go to a doctor. After the usual questions and an examination of pulse, tongue, etc., he forms his diagnosis, searches his brain for a remedy best suited to your ailment and prescribes it for you. In surgery, experts are at hand who may be called in for consultation alone, and who take no part in the performance of an operation.

Now, I want to know this: Why cannot this High Authority plan be applied to the investment business? There ought to be some one of wide experience and established reputation — an expert noted for his care, accuracy and conservatism in such matters — to whom the investor can go and lay down $5, $10, or $25, in exchange for money-making or money- saving advice.’”

- Anonymous, ‘The Ticker’ Magazine (1908)14

This investor’s sentiment from over a century ago echoes those regarding ‘fee only’ advisers and planners today. Even at the turn of the 20th century, investors were mainly interested in paying a flat fee for unbiased investment advice from advisers not conflicted by relationships with third parties.

* * *

The final revolution spawned by the ticker’s invention was the increased customization of investment advice from brokers, advisers, and planners. Harking back to this persistent theme of FinTech and ‘computer code’ empowering advisers since Ancient Mesopotamia, the ticker was another groundbreaking technology that spiked demand for financial advice.

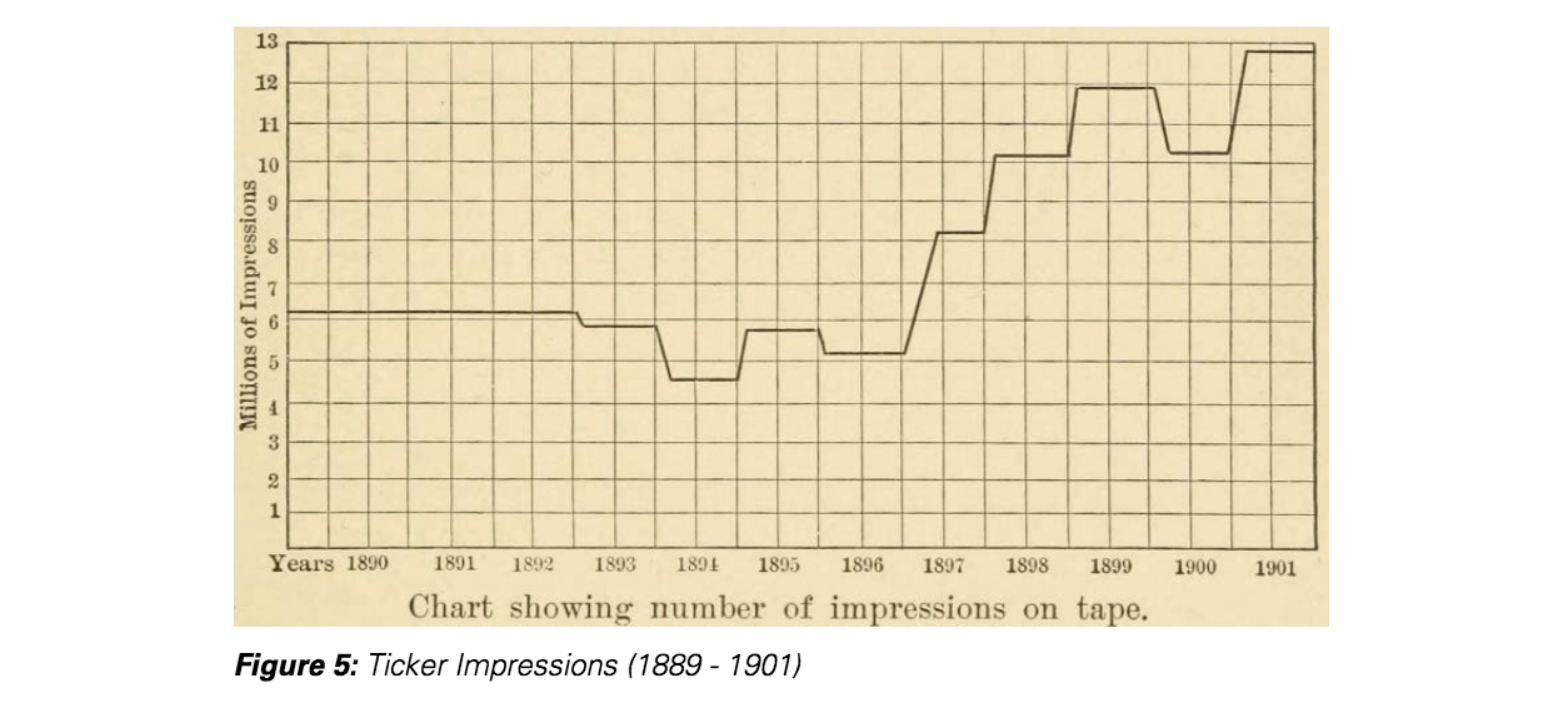

The 1905 publication of ‘Hartfield’s Wall Street Code’ evidenced the impact of this new financial coding language. The speed at which tickers relayed market data required brokers to literally create a new language of short hand jargon and cipher words. The Hartfield book, for example, contained some 467,000 cipher words.15

The power of the code is shown in the chart below, which displays the millions of ticker ‘impressions’ from 1889-1901.16

“The cable-packer, began, by a system of codes, to pack several messages into one. In 1902… 95 per cent of all cable messages are written in codes, so constructed as to make one word do the work of five and even twelve. Elaborate codes have been constructed… [and] one can cable and telegraph to any part of the world”.17

The importance of embracing FinTech was evident to brokers and advisers. In fact, the technology strengthened their relationships with clients:

“An effect of the new transactional language was that investors were bound to their brokers even more closely than before: as an investor, one had to learn a special telegraphic code from the broker's manual, spend as much time as possible in his office and read his chart analyses. Brokerage houses advertised their codes as a sign of seriousness and reliability... a contemporary noticed that Haight & Freese were particularly skilled at attracting new clients by means of free statistics, diagrams and code books.”18

As the above quote references, this new wealth of data enabled brokers and advisers to conduct more intricate research and analysis than previously possible. In turn, clients were given more personalized advice because of brokers’ broader investment knowledge. In 1875, one investor wrote that “it becomes almost a necessity that the broker or operator should consult a table of fluctuations of stocks before he can form an intelligent opinion of future prices”.19 Put simply, people were obsessed with staying up to date on the markets, as the below examples exhibit:

After the release of ticker technology in 1867, the financial services industry was changed irrevocably. Combined advances in telegraphs, cables, and tickers resulted in a broader pool of investors receiving standardized market data on a close to real-time basis.

This overwhelming amount of information led to an increased demand for investment advice from finance professionals. In addition to this spike in business, advisers benefitted from ticker technology as their research capabilities were greatly enhanced by the vast amount of data suddenly at their disposal.

Conclusion

Since the dawn of civilization, people have sought guidance and advice on managing their finances. In Ancient Mesopotamia this meant forecasting the size of your cattle herd, and the monetary value of its ‘dairy yield’. In more recent times, the revolution stemming from the stock ticker’s invention in 1867 necessitated a more prominent role in society for investment advisers and brokers, as people were overwhelmed by the amount of market data suddenly available.

Although these two examples are 4,000 years apart, and the industry has transformed considerably, the importance of FinTech to advisers has been consistent. Across any time period, technology has strengthened the relationships between advisers and clients

Framed within this context, the adviser industry is more exciting than ever, as technology is becoming more advanced by the day. Advisers and financial planners will be equipped with tools to offer their clients much greater levels of customization, in-depth data analytics and more.

The best advisers will continue to operate as their predecessors have, by empowering their practices with technology to better serve their clients.

Footnotes

1 William N. Goetzmann, Money Changes Everything, (Princeton, 2016) pg. 48

2 Goetzmann, Money, pg. 49

3 Goetzmann, Money, pg. 48

4 Ibid, pg. 93

5 Ibid, pg. 93

6 George Rutledge Gibson, The Stock Exchanges of London, Paris, and New York, (New York, 1889) pg. 92

7 Alex Preda, ‘Socio-Technical Agency in Financial Markets: The Case of the Stock Ticker’, Social Studies of Science, Vol. 36, Number 5 (October 2006), pg. 758

8 Ibid, pg. 759

9 Francis Eames, The New York Stock Exchange, (New York, 1894) pg. 51

10 Horace L. Hotchkiss, ‘The Stock Ticker’, The New York Stock Exchange [Edited by Edmund Stedman], (New York, 1905) pg. 433

11 Richard d. Wyckoff, ‘Why You Should Use Charts’, Stock Market Technique, (1934) pg. 16

12 Hotchkiss, ‘The Stock Ticker’, pg. 441

13 Sereno S. Pratt, The Work of Wall Street, (New York, 1903), pg. 140

14 Anonymous, ‘Why Not Investment Experts? Demand for Advice and Opinions on Investments, Suggests the Establishment of a New Profession', The Ticker 1(6) (April 1908) pg. 35.

15 Preda, ‘Socio-Technical Agency’, pg. 766

16 Pratt, Wall Street, pg. 139

17 Pratt, Wall Street, pg. 141

18 Preda, ‘Socio-Technical Agency’, pg. 766

19 Tumbridge & Co., Secret of Success in Wall Street, (New York, 1875) pg. 12

General Legal Disclosures & Hypothetical and/or Backtested Results Disclaimer

The material contained herein is intended as a general market commentary. Opinions expressed herein are solely those of O’Shaughnessy Asset Management, LLC and may differ from those of your broker or investment firm.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by O’Shaughnessy Asset Management, LLC), or any non-investment related content, made reference to directly or indirectly in this piece will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this piece serves as the receipt of, or as a substitute for, personalized investment advice from O’Shaughnessy Asset Management, LLC. Any individual account performance information reflects the reinvestment of dividends (to the extent applicable), and is net of applicable transaction fees, O’Shaughnessy Asset Management, LLC’s investment management fee (if debited directly from the account), and any other related account expenses. Account information has been compiled solely by O’Shaughnessy Asset Management, LLC, has not been independently verified, and does not reflect the impact of taxes on non-qualified accounts. In preparing this report, O’Shaughnessy Asset Management, LLC has relied upon information provided by the account custodian. Please defer to formal tax documents received from the account custodian for cost basis and tax reporting purposes. Please remember to contact O’Shaughnessy Asset Management, LLC, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you want to impose, add, or modify any reasonable restrictions to our investment advisory services. Please Note: Unless you advise, in writing, to the contrary, we will assume that there are no restrictions on our services, other than to manage the account in accordance with your designated investment objective. Please Also Note: Please compare this statement with account statements received from the account custodian. The account custodian does not verify the accuracy of the advisory fee calculation. Please advise us if you have not been receiving monthly statements from the account custodian. Historical performance results for investment indices and/or categories have been provided for general comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your account holdings correspond directly to any comparative indices. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. O’Shaughnessy Asset Management, LLC is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice. A copy of the O’Shaughnessy Asset Management, LLC’s current written disclosure statement discussing our advisory services and fees is available upon request.

Hypothetical performance results shown on the preceding pages are backtested and do not represent the performance of any account managed by OSAM, but were achieved by means of the retroactive application of each of the previously referenced models, certain aspects of which may have been designed with the benefit of hindsight.

The hypothetical backtested performance does not represent the results of actual trading using client assets nor decision-making during the period and does not and is not intended to indicate the past performance or future performance of any account or investment strategy managed by OSAM. If actual accounts had been managed throughout the period, ongoing research might have resulted in changes to the strategy which might have altered returns. The performance of any account or investment strategy managed by OSAM will differ from the hypothetical backtested performance results for each factor shown herein for a number of reasons, including without limitation the following:

▪ Although OSAM may consider from time to time one or more of the factors noted herein in managing any account, it may not consider all or any of such factors. OSAM may (and will) from time to time consider factors in addition to those noted herein in managing any account.

▪ OSAM may rebalance an account more frequently or less frequently than annually and at times other than presented herein.

▪ OSAM may from time to time manage an account by using non-quantitative, subjective investment management methodologies in conjunction with the application of factors.

▪ The hypothetical backtested performance results assume full investment, whereas an account managed by OSAM may have a positive cash position upon rebalance. Had the hypothetical backtested performance results included a positive cash position, the results would have been different and generally would have been lower.

▪ The hypothetical backtested performance results for each factor do not reflect any transaction costs of buying and selling securities, investment management fees (including without limitation management fees and performance fees), custody and other costs, or taxes – all of which would be incurred by an investor in any account managed by OSAM. If such costs and fees were reflected, the hypothetical backtested performance results would be lower.

▪ The hypothetical performance does not reflect the reinvestment of dividends and distributions therefrom, interest, capital gains and withholding taxes.

▪ Accounts managed by OSAM are subject to additions and redemptions of assets under management, which may positively or negatively affect performance depending generally upon the timing of such events in relation to the market’s direction.

▪ Simulated returns may be dependent on the market and economic conditions that existed during the period. Future market or economic conditions can adversely affect the returns.

Composite Performance Summary

For the full composite performance summaries, please follow this link: http://www.osam.com