A True Microcap Strategy

By Jim O’Shaughnessy

March 2016

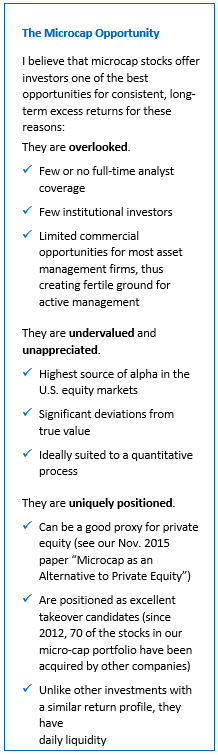

Imagine an undiscovered market where valuations are not systematically picked apart by Wall Street analysts, where huge changes in valuation often go unnoticed, and a stock’s price is very much at odds with its true value. This isn’t a fantasy, because such a market exists today—it is the overlooked stocks with market capitalizations between $50 million and $200 million, commonly known as microcap stocks. This market offers one of the largest opportunities to consistently generate significant excess returns that I have found in all of my research into investment strategies over the course of my career.

What’s more, these opportunities have persisted since I first published What Works on Wall Street 20 years ago. Why? Because the small market cap of these stocks makes them impossible for virtually all professionally-managed portfolios to invest in. Many of these stocks have no analyst coverage and are ignored by both Wall Street and also the financial media. When was the last time you heard anyone on CNBC, Fox Business or Bloomberg talking about a stock with a market cap less than $200 million? When was the last story you read in The Wall Street Journal or Barron’s focusing on stocks with less than $200 million in market cap? In this regard, ignorance leads not to bliss but to highly inefficient pricing. In the current O’Shaughnessy Micro Cap portfolio, nearly half—45 percent—have no analyst coverage and 75 percent are covered by only one or two analysts.

What's more, the lack of analyst coverage often obscures very attractive acquisition candidates. Indeed, since 2012, 70 of the stocks in our Micro Cap portfolio have been acquired by other companies.

If you look at some of the strong-performing stocks the strategy has owned (Table 1), here’s what you’ll see:

To be sure, we have also owned stocks that did poorly and had no analyst coverage, but the point is clear: a lack of coverage often leads to very inefficiently-priced stocks.

Often, these stocks are even overlooked by sophisticated individual investors because they lack access to the tools and data that might help them determine which tiny stocks, out of the thousands available, are the ones that could generate great excess returns. Even with the proper tools, individual investors might lack the ability to put together a portfolio that is diversified enough to tame the higher volatility generated by these tiny stocks.

In today’s market, there are 1,108 microcap stocks in the U.S. with market capitalizations between $50 million and $200 million. These stocks, in aggregate, represent less total market capitalization than Pfizer alone. They are never part of generic asset allocations because capacity is so limited. Large asset managers cannot focus on this area of the market for the same reason—it wouldn’t matter to their bottom line.

Only one ETF—iShares Micro-Cap (ticker: IWC)—tracks the Russell Microcap® Index, which allows investors easy access to this part of the market. But even IWC acts more like a small cap ETF, with a weighted average market cap of $432 million. It is also market cap-weighted, giving the greatest weight to those stocks with the highest market capitalization and gives the lowest weight to the smallest stocks.

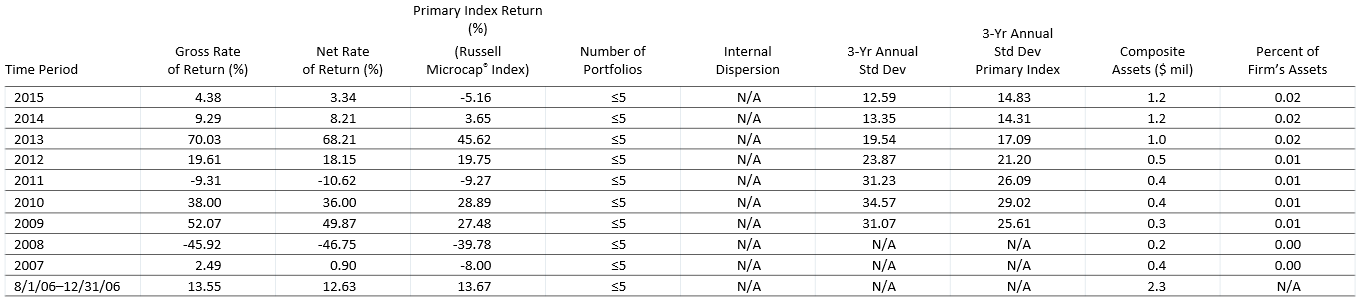

Because of the limited capacity, limited attention, and small size of these companies, the true microcap market has historically proven to be the most fertile ground for active stock selection strategies. Our own strategy, which has been live since 2006, has a 178-percent cumulative return of through December 2015 —higher by 117 percent versus the microcap benchmark over that period.

This paper explores why a disciplined active stock selection strategy can work so well in such a neglected part of the market and how an allocation to this small cap sector can significantly improve the overall results of a portfolio.

Quality Matters, A Lot, in the Microcap Space

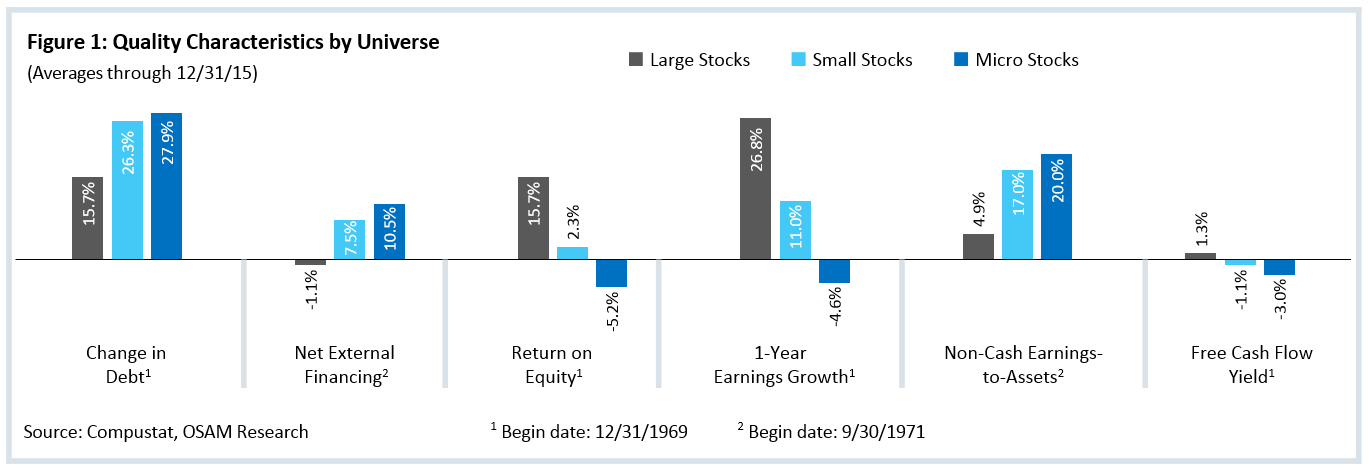

When researching the Microcap Universe, one of the first things you notice is that many tiny stocks have absurdly poor quality. We use two multi-factor composites as the primary measures to ascertain a stock’s quality: Financial Strength, which looks at such things as external financing and one-year change in debt, and Earnings Quality,

which looks at such things as current accruals-to-assets and depreciation-to-CapEx. Figure 1 (below) shows how the average microcap stocks score poorly on quality metrics such as change in debt, net external financing and free cash flow yield. This data reinforces our intuitive understanding of how microcap stocks (i.e., the smallest companies in the market) tend, on average, to be lower-quality and are therefore more susceptible to value traps. For example, although it makes sense for smaller companies to be more reliant on the capital markets for funding, investors should be wary of owning the most levered microcap names. Our selection process eliminates the lowest-scoring third of the universe based on quality, allowing us to focus on the higher-quality stocks instead.

Valuation & Momentum Work Better in the Microcap Universe

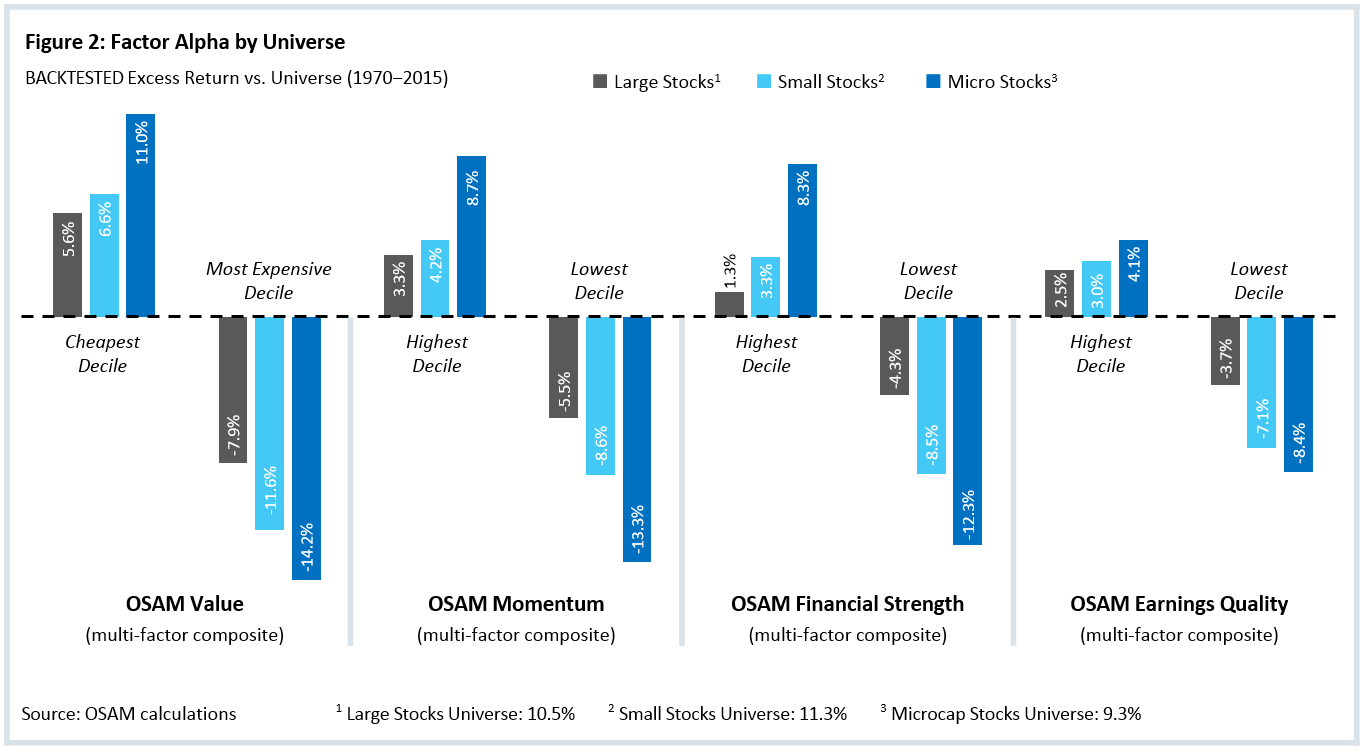

We also eliminate what we believe are the worst companies from the Microcap Universe, using our multi-factor composites for Value and Momentum. Our research shows that it is better to use several factors rather than just one or two when evaluating the relative attractiveness of a stock’s valuation and momentum potential. Therefore, our Value composite ranks a stock on five ratios, including price-to-earnings, price-to-sales, free cash flow-to-enterprise value, and EBITDA-to-enterprise value. We have found that each individual factor comes in and out of favor but that combining all of them gives what we believe is the best indication of a stock’s relative cheapness. The same holds true for Momentum, where we rank a stock on its three-, six-, and nine-month momentum, as well as the 12-month return volatility. This allows us to focus on stocks that not only have good momentum but also have lower volatility overall.

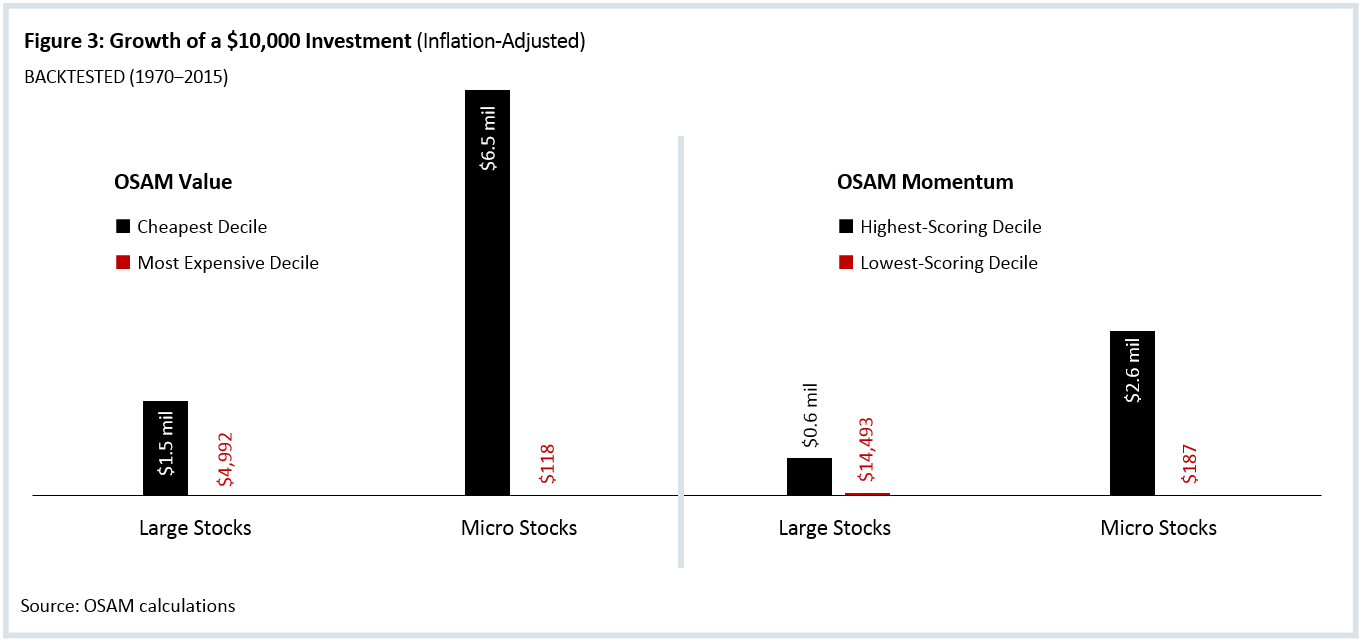

Now that the bottom third of the universe has been eliminated, we then select from the remaining stocks by cheapest Value and highest-scoring Momentum. We do this because we have found that, historically, like our quality measures, our Value and Momentum composites work much better in the microcap space. Figure 2 (below) shows that the cheapest microcap stocks have exhibited much higher excess returns than our Large Stocks Universe (greater than average market cap). Between 1970 and 2015, the inflation-adjusted value of a $10,000 investment in the microcap stocks in the cheapest 10 percent by valuation grows to $6.5 million (see Figure 3, next page). Compare that to a $10,000 investment in the cheapest decile of large stocks, which grew to $1.5 million. The cheapest microcap stocks more than quadruple the real return versus the cheapest large stocks!

What’s more, the spread between the cheapest and most expensive Value decile is much more extreme in micro-cap stocks—$10,000 invested in the most expensive decile of microcap stocks fell to just $118 after accounting for the effects of inflation. In other words, if you consistently invested in the most expensive microcap stocks, the inflation-adjusted value of your initial $10,000 portfolio is essentially worthless. In contrast, $10,000 invested in the most expensive Value decile of large stocks saw $10,000 fall to an inflation-adjusted $4,992—still horrible but not nearly as ghastly as buying the most expensive microcap stocks. The results are not so dramatic when buying the microcap stocks with the highest price momentum—here, your $10,000 grows to an inflation-adjusted $2.7 million. The same investment made in large stocks with strong momentum grew to $609,000 after inflation. We have found that putting the two themes together leads to strong and consistent results.

Putting it All Together

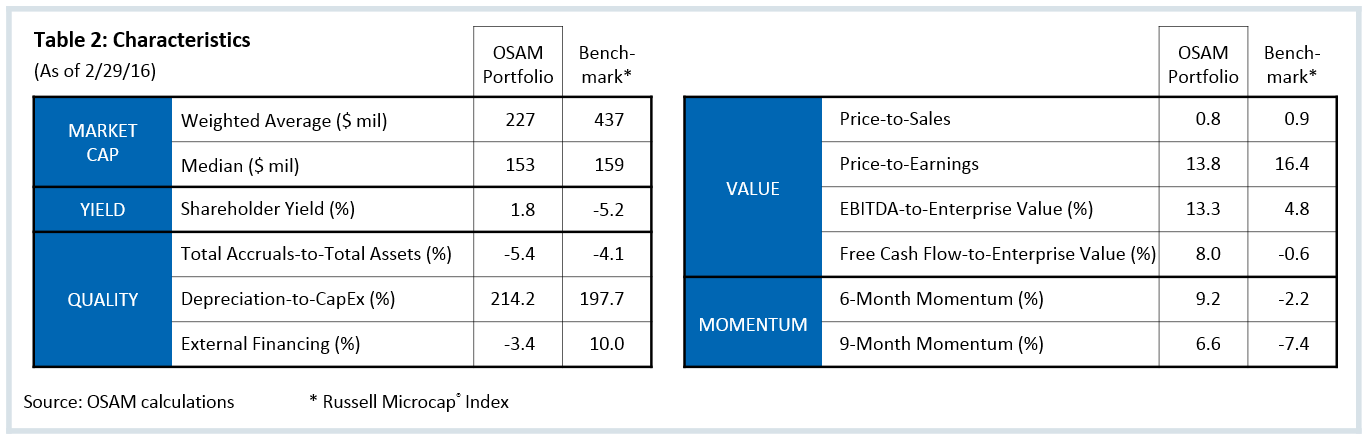

Thus, after starting with approximately 4,600 stocks, we remove the lowest-scoring stocks by Financial Strength, Earnings Quality, Value, and Momentum and then focus on the highest-scoring stocks in Value and Momentum, resulting in a portfolio of approximately 136 stocks (as of 2/29/16). The resulting portfolio has a weighted market cap average of $227 million and a median market cap of $153 million, considerably smaller than both the Russell Microcap® Index and also many of our competitors’ portfolios. As you look at the examples in Table 2 (below), you can see that we create a portfolio of higher-quality, cheap stocks with strong price momentum. As such, we view this portfolio as a Core portfolio comprising the best of Value and Momentum. We believe that the microcap space offers investors one of the best opportunities for consistent, long-term excess returns because they are overlooked, undervalued and unappreciated, and are uniquely positioned.

General Legal Disclosures & Hypothetical and/or Backtested Results Disclaimer

The material contained herein is intended as a general market commentary. Opinions expressed herein are solely those of O’Shaughnessy Asset Management, LLC and may differ from those of your broker or investment firm.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by O’Shaughnessy Asset Management, LLC), or any non-investment related content, made reference to directly or indirectly in this piece will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this piece serves as the receipt of, or as a substitute for, personalized investment advice from O’Shaughnessy Asset Management, LLC. Any individual account performance information reflects the reinvestment of dividends (to the extent applicable), and is net of applicable transaction fees, O’Shaughnessy Asset Management, LLC’s investment management fee (if debited directly from the account), and any other related account expenses. Account information has been compiled solely by O’Shaughnessy Asset Management, LLC, has not been independently verified, and does not reflect the impact of taxes on non-qualified accounts. In preparing this report, O’Shaughnessy Asset Management, LLC has relied upon information provided by the account custodian. Please defer to formal tax documents received from the account custodian for cost basis and tax reporting purposes. Please remember to contact O’Shaughnessy Asset Management, LLC, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you want to impose, add, or modify any reasonable restrictions to our investment advisory services. Please Note: Unless you advise, in writing, to the contrary, we will assume that there are no restrictions on our services, other than to manage the account in accordance with your designated investment objective. Please Also Note: Please compare this statement with account statements received from the account custodian. The account custodian does not verify the accuracy of the advisory fee calculation. Please advise us if you have not been receiving monthly statements from the account custodian. Historical performance results for investment indices and/or categories have been provided for general comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your account holdings correspond directly to any comparative indices. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. O’Shaughnessy Asset Management, LLC is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice. A copy of the O’Shaughnessy Asset Management, LLC’s current written disclosure statement discussing our advisory services and fees is available upon request.

The risk-free rate used in the calculation of Sortino, Sharpe, and Treynor ratios is 5%, consistently applied across time.

The universe of All Stocks consists of all securities in the Chicago Research in Security Prices (CRSP) dataset or S&P Compustat Database (or other, as noted) with inflation-adjusted market capitalization greater than $200 million as of most recent year-end. The universe of Large Stocks consists of all securities in the Chicago Research in Security Prices (CRSP) dataset or S&P Compustat Database (or other, as noted) with inflation-adjusted market capitalization greater than the universe average as of most recent year-end. The stocks are equally weighted and generally rebalanced annually.

Hypothetical performance results shown on the preceding pages are backtested and do not represent the performance of any account managed by OSAM, but were achieved by means of the retroactive application of each of the previously referenced models, certain aspects of which may have been designed with the benefit of hindsight.

The hypothetical backtested performance does not represent the results of actual trading using client assets nor decision-making during the period and does not and is not intended to indicate the past performance or future performance of any account or investment strategy managed by OSAM. If actual accounts had been managed throughout the period, ongoing research might have resulted in changes to the strategy which might have altered returns. The performance of any account or investment strategy managed by OSAM will differ from the hypothetical backtested performance results for each factor shown herein for a number of reasons, including without limitation the following:

- Although OSAM may consider from time to time one or more of the factors noted herein in managing any account, it may not consider all or any of such factors. OSAM may (and will) from time to time consider factors in addition to those noted herein in managing any account.

- OSAM may rebalance an account more frequently or less frequently than annually and at times other than presented herein.

- OSAM may from time to time manage an account by using non-quantitative, subjective investment management methodologies in conjunction with the application of factors.

- The hypothetical backtested performance results assume full investment, whereas an account managed by OSAM may have a positive cash position upon rebalance. Had the hypothetical backtested performance results included a positive cash position, the results would have been different and generally would have been lower.

- The hypothetical backtested performance results for each factor do not reflect any transaction costs of buying and selling securities, investment management fees (including without limitation management fees and performance fees), custody and other costs, or taxes – all of which would be incurred by an investor in any account managed by OSAM. If such costs and fees were reflected, the hypothetical backtested performance results would be lower.

- The hypothetical performance does not reflect the reinvestment of dividends and distributions therefrom, interest, capital gains and withholding taxes.

- Accounts managed by OSAM are subject to additions and redemptions of assets under management, which may positively or negatively affect performance depending generally upon the timing of such events in relation to the market’s direction.

- Simulated returns may be dependent on the market and economic conditions that existed during the period. Future market or economic conditions can adversely affect the returns.

Composite Performance Summary: O’Shaughnessy Micro Cap

Basis of Presentation:

O’Shaughnessy Asset Management, LLC (“OSAM”), founded in 2007, is a Stamford, CT based quantitative money management firm and an SEC Registered Investment Advisor. We deliver a broad range of equity strategies, from micro cap to large cap, and growth to value. Our clients are individual investors, institutional investors, and the high-net-worth clients of financial advisors. James O’Shaughnessy and his team left Bear Stearns to form OSAM in July 2007. All the GIPS® rules of portability were met. Jim maintained continuous management of all accounts during the transition from BSAM to OSAM, which was completed in March 2008. The performance of a past firm or affiliation is being attributed to the performance of the current firm for all the periods starting 1996.

OSAM claims compliance with the Global Investment Performance Standards (GIPS®) and has prepared and presented this report in compliance with the GIPS standards. OSAM has been independently verified for the periods of 2007-2015. BSAM was independently verified in compliance with GIPS 2005-2006 and AIMR-PPS for the periods of 2002 - 2004. The verification reports are available upon request. Verification assesses whether (1) the firm has complied with all the composite construction requirements of the GIPS standards on a firm-wide basis and (2) the firm's policies and procedures are designed to calculate and present performance in compliance with the GIPS standards. Verification does not ensure the accuracy of any specific composite presentation.

A complete list of OSAM’s composite descriptions is available upon request.

The O'Shaughnessy Microcap strategy (the “Composite”) generally seeks to provide long-term appreciation by creating a portfolio of undervalued, microcap companies with solid growth metrics. The strategy identifies companies with market capitalizations that are approximately between $50 million and $200 million. We then limit the universe to the best 2/3 by each of the following composites: Value, Momentum, Earnings Quality, and Financial Strength. From the remaining securities, we select stocks with the best combined Value Composite and Momentum Composite scores. The strategy is periodically rebalanced. Sector weights are a byproduct of the investment process.

Selection Criteria and Valuation Procedures:

The Composite was created in August 2006 and represents the performance of our fee paying, non wrap separately managed accounts invested in the Micro Cap strategy, regardless of asset size. The net of fee return data shown in this presentation represents the reduction of the actual OSAM investment management fee charged. Institutional separate accounts are charged an annual investment advisory fee of 1.50%.

Internal dispersion is calculated using the equal weighted standard deviation of annual gross returns of those portfolios that were included in the composite for the entire year. AUM data is presented from December 31, 2007 forward, consistent with the inception of our firm, and N/A is shown for prior periods. N/A is shown in the “3-Yr Ann Std Dev” field where 36 months of composite performance is not available. All investments are in U.S. equities and all returns are stated in U.S. Dollars. Policies for valuing portfolios, calculating performance, and preparing compliant presentations are available upon request.

Composite Benchmark(s):

The Russell Microcap® Index measures the performance of the microcap segment of the U.S. equity market. It makes up less than 3% of the U.S. equity market. It includes 1000 of the smallest securities in the small-cap Russell 2000® Index based on a combination of their market cap and current index membership.